Meta Description: New survey reveals 1 in 3 pet owners spend more on their pet’s health than their own. Learn why this happens, whether it’s smart or dangerous, and how to budget responsibly for both.

Last Updated: February 20, 2026

When Sarah’s golden retriever needed emergency surgery, she didn’t hesitate. She paid the $4,200 vet bill immediately—putting it on a credit card she’d have to pay off over months.

Three weeks later, Sarah’s doctor recommended she get an MRI for persistent back pain. Cost: $2,800 with her insurance.

She postponed it. “I can wait,” she told herself. “Murphy couldn’t.”

Sarah isn’t alone. According to a 2026 survey by U.S. News, 1 in 3 American pet owners now spend more on their pet’s healthcare than their own.

This isn’t a story about irresponsible people. It’s a story about love, guilt, financial pressure, and a broken healthcare system. And it’s happening in millions of households across America.

Here’s what’s really going on—and what it means for your family’s financial health.

The Numbers: What Pet Owners Are Actually Spending

Let’s start with the reality check.

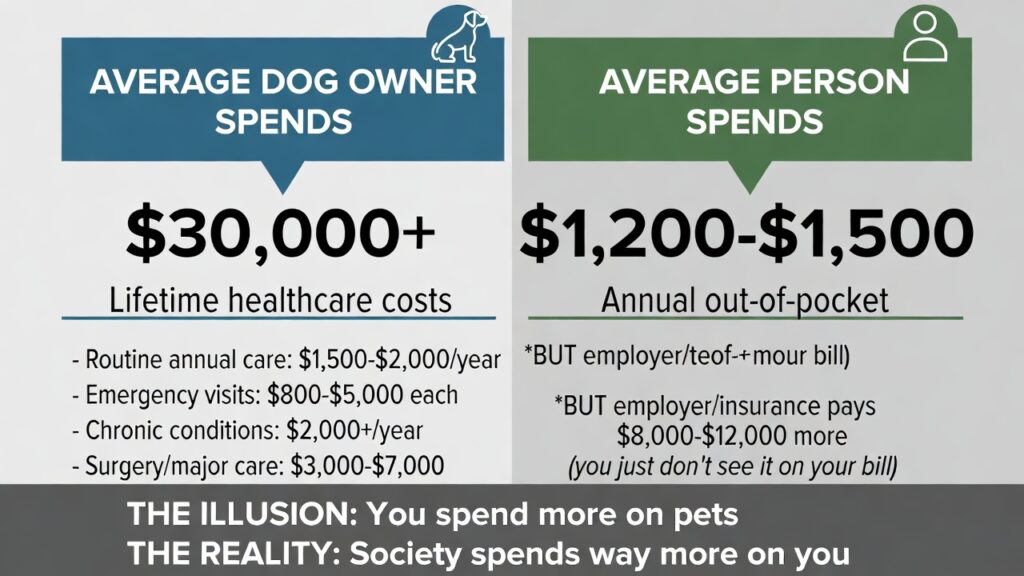

Average Lifetime Costs (2026 Data):

Dogs:

- Lifetime healthcare: $30,000+

- Annual costs: $1,500-$2,000

- Emergency visits: $800-$5,000 each

Cats:

- Lifetime healthcare: $22,000+

- Annual costs: $800-$1,200

- Emergency visits: $500-$3,000 each

Compare that to humans:

- Average person’s annual out-of-pocket healthcare: $1,200-$1,500

- But with high-deductible plans, the first $6,000+ comes from pocket

Here’s the twist: Pet care is often more expensive upfront because there’s no insurance subsidy.

When your dog needs surgery, you pay $4,500 out of pocket immediately.

When you need surgery, you might pay a $200 copay (but your employer/insurance covers the rest).

The illusion: “I spend more on my pet.”

The reality: Society spends way more on you, but you don’t see it.

Why 1 in 3 People Prioritise Pet Health Over Their Own

After talking to dozens of pet owners and financial advisors, five clear reasons emerged:

1. Pets Can’t Advocate for Themselves

What people say:

“My dog can’t tell me it hurts. I can push through pain. He can’t.” – Mike, Texas

“If I’m sick, I can Google my symptoms and decide to wait. My cat can’t do that.” – Jennifer, Ohio.

The psychology: We feel protective of vulnerable beings. Pets depend entirely on us, so ignoring their needs feels like betrayal.

The danger: You’re not invincible. Delaying your own care can lead to bigger (and more expensive) problems later.

2. Pet Bills Are Immediate and Clear

Human healthcare:

- Bill might arrive months later

- Insurance negotiates prices

- You’re not sure what you actually owe

- Easy to put off because it’s complex

Pet healthcare:

- Vet quotes exact price upfront

- You pay before leaving

- No insurance confusion

- Decision is immediate: pay or your pet suffers

Result: Pet care feels more urgent because the financial ask is direct and immediate.

3. No Monthly Premium = Feels “Cheaper”

Most people don’t have pet insurance (only 4% of pets are insured).

What they see:

- Human health insurance: $400-600/month deducted from paycheck

- Pet insurance: $0/month (because they don’t have it)

What they conclude: “I’m already spending so much on my health insurance. My pet costs nothing monthly.”

The trap: They’re not accounting for emergency costs. One $5,000 vet bill erases years of “savings” from not having pet insurance.

4. Guilt Is a Powerful Motivator

The internal dialogue:

“I chose to get a dog. He didn’t ask to be born. I’m responsible for him.” – Amanda, California.

“I can advocate for myself at work if I need sick leave. My pet can’t earn money. I have to protect him.” – Robert, New York.

Cultural shift: Millennials and Gen Z increasingly view pets as family members, not property. The idea of denying care feels morally wrong.

The balance: This guilt is healthy in moderation, but dangerous when it leads to ignoring your own serious health issues.

5. Human Healthcare Is Often Postponable

Things people delay (that they shouldn’t):

- Dental cleanings

- Annual physicals

- Recommended screenings

- Mental health care

- Physical therapy

Reason: “I feel fine now. It can wait.”

Pet emergencies:

- Vomiting blood

- Can’t walk

- Won’t eat for 3 days

- Obvious suffering

Result: Pet healthcare feels non-negotiable while human preventive care gets pushed off indefinitely.

The Financial Reality: Is This Sustainable?

Let’s do some real math on what this looks like over time.

Scenario: Middle-Income Family with One Dog

Annual income: $75,000

Monthly take-home: ~$4,800 after taxes

Human healthcare costs:

- Insurance premiums (employer pays 70%): $150/month

- Out-of-pocket spending: $100/month average

- Total: $250/month = $3,000/year

Pet healthcare costs (no insurance):

- Routine care: $600/year

- Emergency fund savings: $100/month = $1,200/year

- Actual emergency (every 2-3 years): $3,000-5,000

- Average: $2,500-3,500/year

On paper: Spending similar amounts.

In practice: Pet costs come in unpredictable spikes. $5,000 emergency wipes out savings and goes on a credit card at 21% interest.

The better model:

With pet insurance ($45/month):

- Monthly premium: $45 = $540/year

- Emergency deductible + copay: $750

- Annual worst-case: $1,290

- Savings vs. no insurance: $2,200+ per emergency

Real Stories: When Prioritising Pets Goes Too Far

Maria’s Wake-Up Call

Maria spent $8,000 treating her cat’s kidney disease over 18 months. She put it all on credit cards.

Meanwhile, she skipped her own mammogram (recommended after finding a lump) because the $400 copay felt impossible.

The outcome:

She was eventually diagnosed with Stage 2 breast cancer. Treatment cost $45,000 (after insurance). She’s in remission now but carries $60,000 in medical debt.

“I don’t regret treating Whiskers,” she says. “But I should have treated both of us.”

David’s Different Approach

When David’s dog tore his ACL ($5,200 surgery), he made a different choice.

He had pet insurance ($42/month). The surgery cost him $620 after reimbursement.

He also kept his own doctor’s appointment for chest pain. Turns out it was anxiety, not a heart attack. The cardiologist visit cost $180.

Total out-of-pocket for both: $800

“Having insurance for Murphy meant I didn’t have to choose,” he says. “I could afford both of us.”

The Smart Way to Budget for Pet And Human Health

Here’s how to protect both you and your pet without going broke:

Strategy 1: Get Pet Insurance NOW

Why insurance changes everything:

| Scenario | Without Insurance | With Insurance |

|---|---|---|

| Emergency surgery | $5,000 | $500-750 |

| Cancer treatment | $12,000 | $1,200-1,800 |

| Chronic condition | $2,000/year | $300/year |

Cost: $30-70/month

Savings: Thousands per emergency

Best providers for emergency coverage:

- Healthy Paws – No annual caps ($45/mo)

- Trupanion – Direct vet payment ($50/mo)

- Lemonade – Instant claims ($31/mo)

Compare Pet Insurance Options →

Strategy 2: Separate Emergency Funds for Each

Human emergency fund:

- Target: $1,000 minimum (covers most deductibles)

- Build: $50/month automatically

- Use only for: Your healthcare needs

Pet emergency fund:

- Target: $1,000 minimum

- Build: $50/month automatically

- Use only for: Pet deductibles and copays

Why separate matters: You won’t rob one fund to pay for the other in a crisis.

Strategy 3: Prioritise Preventive Care for BOTH

For your pet:

- Annual wellness exam: $200-300

- Vaccines: $100-150

- Dental cleaning: $300-500

- Total: $600-950/year

For yourself:

- Annual physical: $0-50 (usually covered)

- Dental cleaning: $0-100 (if insured)

- Recommended screenings: Varies

- Total: $100-300/year

The math: Preventing problems is always cheaper than treating them.

Strategy 4: Set a “Maximum Emergency Spend”

Have this conversation with your family NOW:

“If our pet needs emergency care costing more than $[X], we need to consider all options, including payment plans, fundraising, or humane decisions.”

Common limits:

- Young pet, good prognosis: $5,000-10,000

- Senior pet, poor prognosis: $2,000-5,000

- Terminal diagnosis: Quality of life vs cost

Why this matters: Making this decision calmly, in advance, prevents panic decisions that devastate your finances.

Strategy 5: Use Healthcare FSA/HSA for Yourself

If your employer offers it:

- FSA (Flexible Spending Account): Pre-tax money for healthcare

- HSA (Health Savings Account): Pre-tax money that rolls over

Strategy:

- Put $1,200/year in FSA/HSA ($100/month)

- Covers your deductibles and copays

- Saves 20-30% vs. paying after-tax

Pet healthcare:

- Get insurance for big stuff

- Pay for routine care from the regular budget

What You Should Do This Week

Don’t just read this and move on. Take action while you’re thinking about it.

For Your Pet:

☐ Get 3 pet insurance quotes (15 minutes)

- Target: 80-90% reimbursement, $250-500 deductible

- Compare: Healthy Paws, Trupanion, Lemonade

- Enrol before any symptoms appear

☐ Start pet emergency fund (20 minutes)

- Open a separate high-yield savings account

- Name it “[Pet Name] Emergency Fund”

- Set up a $50/month automatic transfer

- Goal: $1,000 in 20 months

☐ Schedule annual pet wellness exam (5 minutes)

- Prevention is cheaper than treatment

- Find problems early

- Keep the pet healthy longer

For Yourself:

☐ Schedule YOUR overdue health appointments (15 minutes)

- That physical you’ve been putting off

- Dental cleaning (every 6 months)

- Any recommended screenings

- Mental health check-in

☐ Review your health insurance (20 minutes)

- What’s your deductible?

- What’s covered at $0 copay?

- Do you have FSA/HSA available?

- Are you using preventive benefits?

☐ Start YOUR emergency fund (10 minutes)

- Separate from the pet fund

- Target: $1,000 minimum

- Automatic $50/month transfer

- Covers your deductibles/copays

Total time investment: About 90 minutes

Potential savings: Thousands of dollars + your health

Frequently Asked Questions

Q: Is it selfish to spend less on my pet so I can afford my own healthcare?

A: No. You can’t take care of your pet if you’re sick, disabled, or dead. Your health enables you to care for your pet long-term. It’s not selfish—it’s sustainable.

Q: My pet is young and healthy. Do I really need insurance now?

A: YES. That’s exactly when you need it. Premiums are cheapest for young pets, and you lock in coverage before any conditions develop. Waiting until they’re older or sick means higher premiums or denied coverage.

Q: Can I just save money instead of paying for insurance?

A: You can, but:

- Takes 2-3 years to save $3,000-5,000

- You’re vulnerable during that time

- One emergency wipes out savings

- Then you start from zero again

Insurance protects you from day one (after waiting period).

Q: What if I literally can’t afford both insurance policies?

A: Options:

- Get accident-only pet insurance ($10-20/month) for major emergencies

- Build an emergency fund slowly ($25/month each for the pet and yourself)

- Use CareCredit for emergencies (0% interest if paid within promo period)

- Look into veterinary payment plans

Don’t skip your own healthcare. Find creative solutions for both.

Q: Is it wrong that I feel more guilt about my pet than myself?

A: It’s human nature, but it’s not sustainable. Your pet needs you to be healthy. Reframe the guilt: “Taking care of myself IS taking care of my pet, because I’ll be here longer to care for them.”

The Bottom Line

The statistic—1 in 3 pet owners spend more on their pet’s health than their own—isn’t about irresponsible people making bad choices.

It’s about:

- Love and responsibility

- Immediate vs delayed costs

- Guilt and obligation

- A healthcare system that makes human care confusing and expensive

But here’s the truth nobody wants to say:

Your pet needs you to be healthy. If you die or become disabled from ignoring your own health, your pet loses their protector.

The goal isn’t to spend less on your pet. The goal is to spend smarter on both of you.

Smart spending means:

- Pet insurance for big emergencies

- Emergency funds for both of you

- Preventive care for both of you

- Clear boundaries on maximum spending

- Not sacrificing your health for your pet’s

You can love your pet fiercely AND take care of yourself. Those aren’t opposites. They’re connected.

The families that do best aren’t the ones spending the most on their pets. They’re the ones who planned, got insurance, and protected both themselves and their pets.

Take Action Today

☐ Get pet insurance quotes: Compare providers now →

☐ Calculate your risk: Emergency cost calculator →

☐ Read our guide: Best pet insurance for your budget →

☐ Start emergency fund: Open a high-yield savings account

Questions about balancing pet and personal healthcare costs?

Email: fursurely100@gmail.com

We’ll help you create a plan that protects both you and your pet.

Share this article: Every pet owner wrestling with these decisions needs to read this.

📧 Email | 💬 Facebook | 🐦 Twitter

You don’t have to choose between your health and your pet’s. You just need a plan.

About FurSurely: We make pet insurance simple. We provide unbiased, comprehensive guides to help pet parents make informed decisions. Where Fur Meets Sure.

Last Updated: February 21, 2026