Meta Description: Pet insurance premiums jumped 20% in 2026. Discover why costs spiked, which providers raised rates the most, and 5 proven strategies to lower your bill without losing coverage.

Last Updated: February 24, 2026

Rachel opened her February renewal notice and stared at the number in disbelief.

New monthly premium: $63

She’d been paying $52 last year. That is a 21.15% increase for the same coverage. Same deductible. Same reimbursement rate. Nothing changed except the price. Rachel isn’t being punished, and she definitely isn’t alone.

According to the latest NAPHIA (North American Pet Health Insurance Association) 2026 data, pet insurance premiums increased an average of 20% across the industry over the last 12 months. This represents the largest single-year jump in a decade. If your renewal notice caused immediate “sticker shock,” this guide explains the market forces at play and provides a step-by-step blueprint to reduce your costs.

If you’re wondering whether insurers can legally raise your rates, read our breakdown of state-level pet insurance regulations in 2026.

The 2026 Price Reality: Dogs vs. Cats

The “20% average” hides the volatility occurring in specific regions and breeds. While the national average for a dog sits around $55/month, your specific geography dictates your “inflation tax.”

Monthly Premium Averages (February 2026)

If you live in California, New York, or Florida, you likely saw increases closer to 23-26%. This is due to a combination of higher labor costs for veterinary technicians and increased property insurance for vet clinics, which is passed down to the consumer.

To understand how these increases compare to real emergency bills, see The $5,000 Vet Visit: What Most Owners Learn Too Late.

5 Reasons Your Premiums Exploded in 2026

Insurance companies are regulated by state departments, meaning they can’t just raise rates on a whim. They must prove their “loss ratios” (claims paid vs. premiums collected) justify the hike. Here is why they won those arguments this year:

1. Advanced “Human-Grade” Veterinary Care

We are no longer in the era of “wait and see.” In 2026, 3D-printed orthopedic implants, personalized oncology (cancer) vaccines, and MRI-guided surgeries are standard.

The Cost: A standard MRI for a dog now averages $3,200, up from $2,600 two years ago.

The Impact: As life-saving tech becomes more available, owners use it more frequently, leading to massive payouts for insurers.

2. The “Shortage” Surcharge

There is a critical shortage of veterinary specialists in the U.S. To retain staff, clinics have hiked salaries by 15-20% since 2024.

Expert Note: “When a clinic’s overhead for staff and specialized equipment rises, the ‘usual and customary’ fee for a simple ear infection or a complex surgery rises in tandem,” says Dr. Aris Messinis, a veterinary consultant.

3. Corporate Consolidation

Over 30% of U.S. veterinary practices are now owned by large corporations or private equity firms. These entities often have higher profit margin requirements than independent “mom-and-pop” shops, leading to more aggressive billing for diagnostic tests.

4. Climate-Driven Claims

2025 was a record year for environmental health claims. From tick-borne illnesses spreading into new northern territories to respiratory issues from wildfire smoke in the West, “environmental” claims rose 18% year-over-year.

5. Adverse Selection

As premiums rise, healthy pet owners often drop their coverage, while owners of pets with chronic issues keep theirs. This leaves the insurance company with a “sick” pool of pets, forcing them to raise rates even higher to stay solvent.

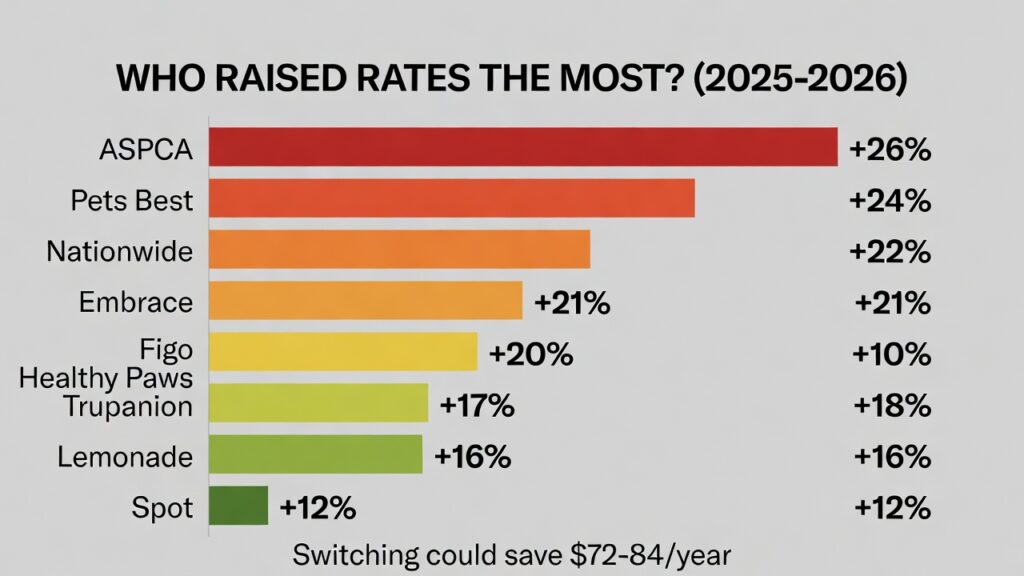

Provider Comparison: Who Raised Rates the Most?

Not all providers are reacting to inflation the same way. Some have used technology to keep overhead low, while others have passed every penny of inflation to the customer.

Real-World Claims: The Math of 2026

To understand if insurance is still “worth it” at $63/month, you have to look at the current cost of emergencies.

Case Study 1: The “Counter Surfer” (Labrador Retriever)

Incident: Ingested a corn cob, causing intestinal blockage.

2024 Cost: $3,800

2026 Cost: $4,550

Insurance Payout (90% Reimbursement / $500 Deductible): $3,645

Owner’s Out-of-Pocket: $905

Verdict: One incident covers 4.8 years of premiums at current rates.

Case Study 2: The Chronic Condition (French Bulldog)

Incident: Brachycephalic Obstructive Airway Syndrome (BOAS) Surgery.

2026 Cost: $6,200

Insurance Payout (80% Reimbursement / $250 Deductible): $4,760

Owner’s Out-of-Pocket: $1,440

Verdict: This breed is seeing the highest premium hikes (often $120+/month) because of high-claim probability.

Red Flags & Consumer Protections: What to Watch For

Before you switch providers to save $15/month, you must be aware of the “Fine Print Traps” that have become common in 2026:

Bilateral Exclusions: If your pet had a ligament tear in the left leg, some insurers will exclude the right leg entirely if you switch to them.

Vague “Pre-existing” Language: Look for companies that “curate” pre-existing conditions. For example, some will cover a condition if the pet has been “symptom-free” for 180 days.

Payout Caps: In 2026, a $5,000 annual cap is a danger zone. With surgeries hitting $6,000+, you want an unlimited or at least $10,000 annual limit.

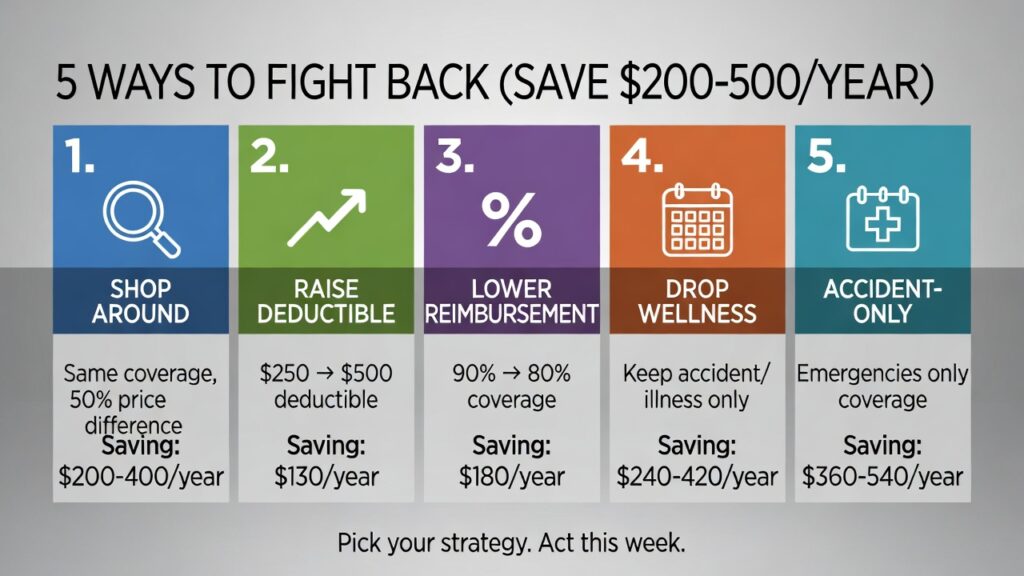

5 Proven Strategies to Lower Your Bill

1. The “Deductible Dial.”

Increasing your annual deductible from $250 to $750 can often slash your premium by 25-30%.

Strategy: Use the savings to fund a dedicated “Pet Savings Account.” You only pay the $750 if an emergency happens, but you save the premium every single month.

2. Drop the “Wellness” Add-on

Most wellness plans are simply “pre-paid” vet visits.

The Math: If your wellness rider costs $25/month ($300/year) but only pays out $250 in routine vaccines and exams, you are losing $50/year for the “convenience.” Drop it and pay the vet directly.

3. Adjust the Reimbursement Level

Moving from 90% to 80% reimbursement is often the difference between a $70 premium and a $50 premium. You are still protected against a $10,000 disaster, but you take on an extra 10% of the risk.

4. Multi-Pet Discounts

Many providers (like Spot and Pumpkin) offer 10% discounts for the second pet. If your pets are split across two different companies, consolidating them usually yields immediate savings.

5. Consider “Accident-Only” for Seniors

If your 12-year-old dog has multiple pre-existing conditions (arthritis, kidney issues), a comprehensive plan is likely $150+/month and won’t cover his existing meds. Switching to an Accident-Only plan ($15-20/month) protects you if he gets hit by a car or eats a toxin, while you self-fund his known illnesses.

Breed-Specific Considerations for 2026

Alternatives to Traditional Insurance

If the 20% hike makes insurance impossible for your budget, consider these “safety nets”:

High-Yield Savings Account (HYSA): Automate a $50/month transfer.

Veterinary Discount Plans: (e.g., PetAssure) These offer 25% off in-house services for a flat monthly fee with no exclusions.

Credit Lines: CareCredit or Scratchpay offer 0% interest for 6-12 months on vet bills.

FAQ: Your 2026 Premium Questions Answered

Q: Can I negotiate my rate with my current provider? A: Generally, no. Rates are filed with the state. However, you can negotiate your “coverage levels” (deductible/reimbursement) to lower the price.

Q: If I switch, will my pet’s current allergies be covered? A: No. Any condition documented in vet records before the new policy’s 14-day waiting period will be considered pre-existing.

Q: Why is my neighbor’s rate lower for the same breed? A: Pet insurance is hyper-local. Even a different zip code within the same city can change the rate based on the proximity to expensive 24/7 emergency hospitals.

Q: Is “Direct Pay” worth the higher premium? A: In 2026, yes. With the average emergency bill crossing $2,000, many owners don’t have the credit limit to pay upfront and wait for reimbursement.

Final Verdict: Should You Keep Your Policy?

Despite the 20% jump, pet insurance remains a vital tool for 80% of owners. Unless you have $5,000 in liquid cash specifically set aside for your pet, the risk of “economic euthanasia”—having to put a pet down because you can’t afford the cure—is too high in this inflationary environment.

Your Next Steps:

Audit your renewal: Check your increase percentage. If it’s over 20%, it’s time to shop.

Get 3 Quotes: Compare Spot, Pumpkin, and Lemonade for a baseline.

Adjust your deductible: See how a $500 or $750 deductible changes your monthly math.