Meta Description: Only 1 in 4 Americans has pet insurance despite 15% premium increases. Compare the top 5 providers (ASPCA, MetLife, Spot, Pumpkin, Lemonade) with real claim examples and breed-specific costs.

Last Updated: February 26, 2026

Executive Summary

As of February 2026, the U.S. pet healthcare market is at a crossroads. While veterinary medicine has reached “human-grade” sophistication—offering everything from targeted oncology to advanced neurology—the financial burden has shifted dramatically. U.S. pet insurance premiums jumped 20% in 2025-2026, driven by veterinary cost inflation and the consolidation of practices by private equity.

Currently, only 1 in 4 Americans has an established financial safety net (either through insurance or dedicated savings) for pet emergencies. With emergency surgeries for common issues like gastric torsion or spinal ruptures now regularly exceeding $5,000, insurance is no longer a luxury but a critical tool for financial resilience.

This guide breaks down the top-rated providers to help you navigate this high-cost environment.

The 2026 “1 in 4” Reality: Market Analysis

Despite a record-breaking $5.6 billion in gross written premiums in North America, only 4% of the total U.S. pet population is insured. This “protection gap” means that most owners are one accident away from “economic euthanasia”—the heartbreaking decision to end a pet’s life because of an unaffordable bill.

Current Market Snapshot:

Average Premiums (2026):

- Dogs (Accident & Illness): $43-70/month (depending on breed, age, location)

- Cats (Accident & Illness): $23-35/month

The Critical Gap:

- Insured pets: 4% (roughly 3.2 million pets)

- Uninsured pets: 96% (roughly 77 million pets)

- Americans with NO financial safety net: 75% (3 in 4)

The Trend: Cat insurance is the fastest-growing segment, with feline enrollments increasing by 23% as owners recognize the high cost of chronic kidney disease ($3,000-5,000) and urinary obstructions ($2,000-4,000).

Why premiums jumped 20% in 2025: Veterinary costs increased 11%, more pets are insured and filing claims, and advanced treatments (MRI, chemotherapy, stem cell therapy) are now standard care. Read the full breakdown of the 20% increase →

Top 5 Pet Insurance Providers for February 2026

1. ASPCA Pet Health Insurance: Best for Holistic Care

ASPCA continues to lead the 2026 rankings due to its “Complete Coverage” plan, which includes dental illnesses, behavioral modification, and alternative therapies (acupuncture, hydrotherapy) as standard features.

Monthly Cost:

- Dogs: $45-75 (average $58)

- Cats: $25-40 (average $32)

Why it’s Top-Rated:

- ✅ Covers “curable” pre-existing conditions if the pet remains symptom-free for 180 days

- ✅ Dental illness included (most exclude this)

- ✅ Behavioral modification coverage (anxiety, aggression training)

- ✅ Alternative therapies covered

- ✅ Horses can be added to the policy

Best for:

- Senior pets

- Breeds prone to periodontal disease

- Owners seeking comprehensive wellness

Downsides:

- Higher premiums than budget options

- 14-day waiting period for all conditions

2. MetLife Pet Insurance: Best for Multi-Pet Households

MetLife has disrupted the market with a unique shared deductible model. Instead of paying three separate deductibles for three pets, you can aggregate bills toward a single limit.

Monthly Cost:

- Dogs: $40-65 (average $52)

- Cats: $22-35 (average $28)

Why it’s Top-Rated:

- ✅ Zero-day waiting period for accidents (coverage starts at midnight on sign-up day)

- ✅ Shared deductible across multiple pets

- ✅ First responder discounts (10-15% for police, fire, military)

- ✅ No upper age limit for enrollment

Best for:

- Households with 2+ animals

- First responders and military families

- Pets prone to accidents (active breeds)

Downsides:

- 14-day waiting period for illnesses

- Orthopedic conditions have a 6-month wait

3. Spot Pet Insurance: Best for High-Limit Security

Spot stands out for its unlimited annual payout options and its 24/7 telehealth line, which helps owners avoid expensive $200+ after-hours ER exam fees for minor concerns.

Monthly Cost:

- Dogs: $38-62 (average $48)

- Cats: $20-32 (average $26)

Why it’s Top-Rated:

- ✅ Unlimited annual coverage option (no caps)

- ✅ Claims processed in under 3.3 days on average

- ✅ 24/7 telehealth line (can save $200+ ER visit)

- ✅ 270-day window to file claims (most allow only 90-180 days)

- ✅ Gold Plan includes wellness/preventive care

Best for:

- Owners who want “blanket” protection with no annual caps

- Breeds prone to expensive chronic conditions

- Anyone who wants fast claim processing

Downsides:

- Premiums in mid-range (not cheapest)

- Unlimited coverage adds to the monthly cost

4. Pumpkin Pet Insurance: Best for Predictable Reimbursement

Pumpkin keeps it simple by defaulting to a 90% reimbursement rate for all plans, ensuring minimal out-of-pocket stress during a crisis.

Monthly Cost:

- Dogs: $55-85 (average $68)

- Cats: $28-42 (average $35)

Why it’s Top-Rated:

- ✅ 90% reimbursement standard (you pay only 10%)

- ✅ No upper age limits for enrollment

- ✅ Excellent coverage for hereditary conditions from day one

- ✅ Preventive Essentials pack available

- ✅ “PumpkinNow” urgent pay feature (15-minute reimbursement for large bills)

Best for:

- Puppies and kittens

- Pedigree breeds with known genetic risks

- Owners who want high reimbursement rates

- Anyone needing fast emergency reimbursement

Downsides:

- Higher premiums (trade-off for 90% reimbursement)

- Annual limits cap at $20,000 (not unlimited)

5. Lemonade Pet Insurance: Best for Tech-Savvy Savings

Lemonade offers the most affordable rates in the 2026 market, with plans starting as low as $12/month for cats.

Monthly Cost:

- Dogs: $25-45 (average $35)

- Cats: $15-25 (average $20)

Why it’s Top-Rated:

- ✅ Lowest premiums in the industry

- ✅ AI-driven claims bot can approve and pay claims in minutes

- ✅ Bundle discounts (pair with Lemonade home/renters insurance)

- ✅ 2-day waiting period for accidents (vs 14 days elsewhere)

- ✅ 100% digital experience (no phone calls, no paperwork)

Best for:

- Budget-conscious owners

- Tech-savvy users who prefer mobile-first

- Young, healthy pets (lock in low rates)

- Anyone wanting instant claim decisions

Downsides:

- Annual cap at $100,000 (high but not unlimited)

- Less comprehensive than ASPCA or Spot for specialty care

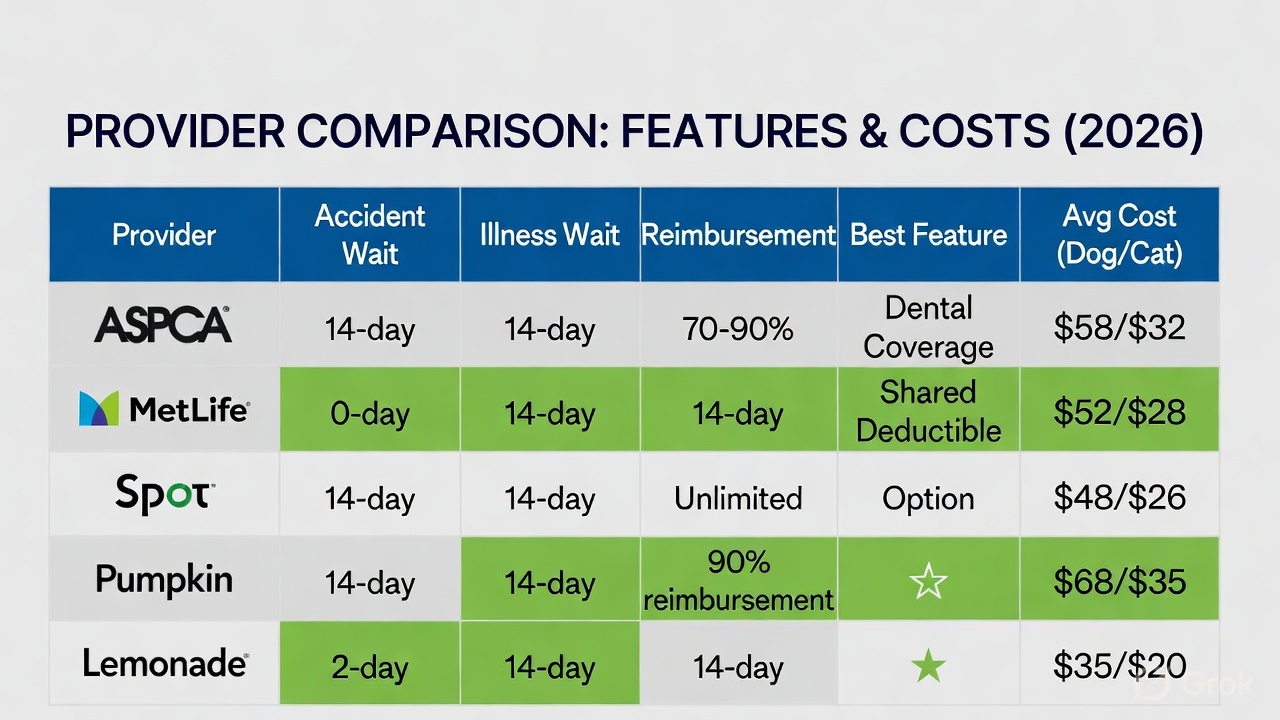

Comparing the Leaders: Feature Breakdown

| Provider | Accident Wait | Illness Wait | Reimbursement | Annual Limit | Best Feature | Avg Monthly (Dog/Cat) |

|---|---|---|---|---|---|---|

| ASPCA | 14 days | 14 days | 70-90% | $2.5K-Unlimited | Holistic coverage; Dental included | $58 / $32 |

| MetLife | 0 days | 14 days | 70-90% | $2K-Unlimited | Shared deductible for multi-pet | $52 / $28 |

| Spot | 14 days | 14 days | 70-90% | Unlimited | 24/7 Telehealth; Fast claims (3.3 days) | $48 / $26 |

| Pumpkin | 14 days | 14 days | 90% | $20K | High reimbursement; Urgent pay (15 min) | $68 / $35 |

| Lemonade | 2 days | 14 days | 70-90% | $100K | Lowest cost; AI instant approval | $35 / $20 |

Key Takeaways:

- Cheapest: Lemonade ($35 dogs, $20 cats)

- Fastest accident coverage: MetLife (0-day wait)

- Highest reimbursement: Pumpkin (90% standard)

- No caps: Spot (unlimited option)

- Most comprehensive: ASPCA (dental, behavioral, alternative therapies)

The Math of Protection: Real Claim Examples

To understand why “1 in 4” owners choose insurance despite rising premiums, look at the math for these common 2026 veterinary scenarios.

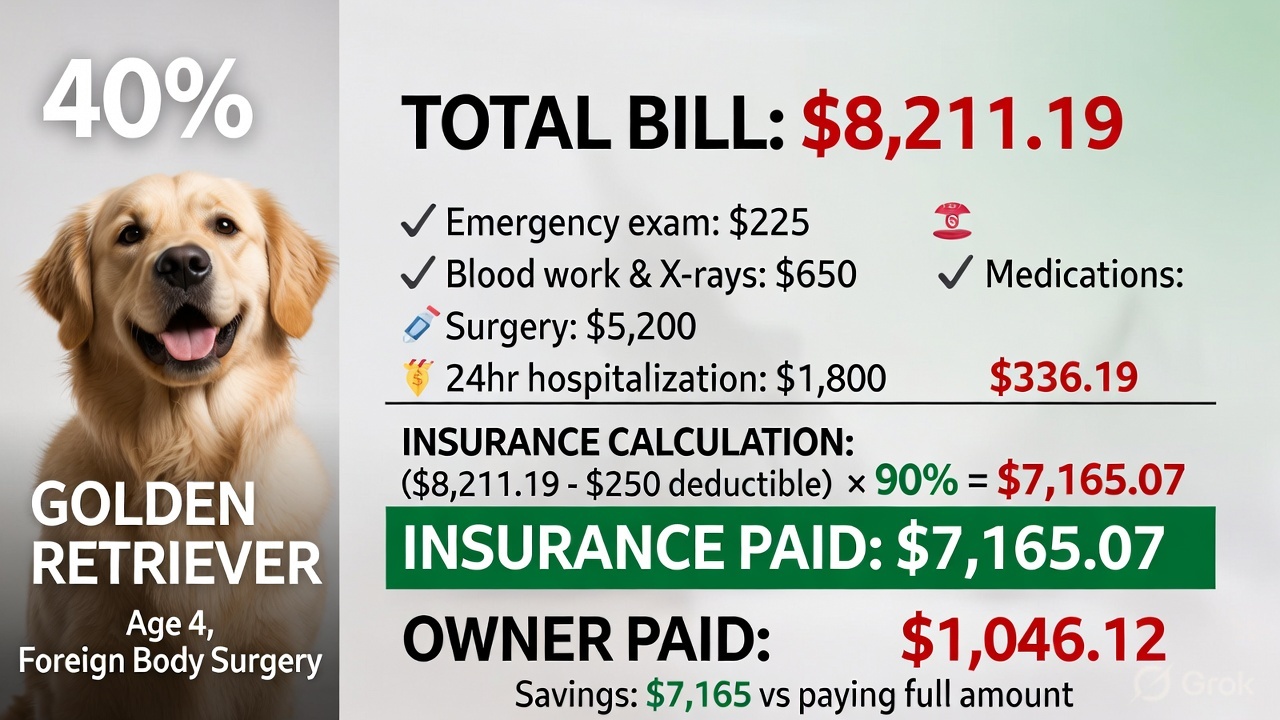

Scenario A: Foreign Body Surgery (Golden Retriever)

What happened: The dog ate a chew toy that lodged in the intestines

Total Bill: $8,211.19

- Emergency exam: $225

- Blood work & X-rays: $650

- Surgery (foreign body removal): $5,200

- 24-hour hospitalization: $1,800

- Medications: $336.19

Policy Details:

- Deductible: $250

- Reimbursement: 90%

The Math:

($8,211.19 - $250) × 0.90 = $7,165.07

Insurance Paid: $7,165.07

Owner Paid: $1,046.12

Savings vs No Insurance: $7,165.07

With Pumpkin (90% standard): Same result

With Lemonade (80% option): Insurance pays $6,369, you pay $1,842

Without Insurance: You pay $8,211.19

Scenario B: Urinary Blockage (Indoor Cat)

What happened: Male cat unable to urinate (FLUTD – life-threatening emergency)

Total Bill: $3,000

- Emergency exam: $175

- Catheterization: $800

- Labs & bloodwork: $450

- Anesthesia: $400

- Hospitalization (48 hours): $950

- Medications: $225

Policy Details:

- Deductible: $500

- Reimbursement: 80%

The Math:

($3,000 - $500) × 0.80 = $2,000

Insurance Paid: $2,000

Owner Paid: $1,000

Savings vs No Insurance: $2,000

Without Insurance: You pay $3,000 (entire emergency fund wiped out)

Scenario C: Cancer Treatment (Labrador)

What happened: A 7-year-old Lab diagnosed with lymphoma

Total Treatment Cost (8 months): $14,800

- Initial diagnosis & staging: $2,200

- Chemotherapy (6 cycles): $10,500

- Follow-up exams & labs: $1,600

- Supportive medications: $500

Policy Details:

- Deductible: $500 (annual, one-time)

- Reimbursement: 90%

- Annual limit: Unlimited (Spot) or $100K (Lemonade)

The Math:

($14,800 - $500) × 0.90 = $12,870

Insurance Paid: $12,870

Owner Paid: $1,930

Savings vs No Insurance: $12,870

Without Insurance: You pay $14,800 OR make an impossible decision to forgo treatment.

This is why unlimited coverage matters: Cancer treatment easily exceeds $10K-20K

Breed-Specific Financial Risks

Your pet’s DNA is the biggest predictor of your lifetime insurance cost. Insurers adjust rates based on the high probability of specific claims.

High-Risk (Expensive) Breeds:

English/French Bulldogs:

- Risk: Brachycephalic airway syndrome, hip dysplasia, cherry eye

- Surgery costs: $3,000-7,000

- Average premium: $75-95/month

- Lifetime healthcare: $30,000-40,000

German Shepherds:

- Risk: Hip dysplasia, degenerative myelopathy, bloat

- Surgery costs: $4,000-8,000 (hip replacement)

- Average premium: $55-75/month

- Lifetime healthcare: $25,000-35,000

Golden Retrievers:

- Risk: Cancer (lymphoma, hemangiosarcoma), hip dysplasia

- Treatment costs: $10,000-20,000 (cancer)

- Average premium: $50-70/month

- Lifetime healthcare: $30,000+

Dachshunds:

- Risk: IVDD (intervertebral disc disease) – 25% will experience

- Surgery costs: $8,000-12,000

- Average premium: $45-60/month

- Lifetime healthcare: $20,000-30,000

Maine Coon Cats:

- Risk: Hypertrophic cardiomyopathy (HCM), hip dysplasia

- Treatment costs: $2,000-5,000 annually

- Average premium: $40-55/month

- Lifetime healthcare: $15,000-25,000

Lower-Risk (Affordable) Breeds:

Mixed Breeds (Dogs):

- Average premium: $35-50/month

- Hybrid vigor: Generally healthier than purebreds

Domestic Shorthair Cats:

- Average premium: $20-30/month

- Fewer genetic issues than pedigree cats

Border Collies / Australian Shepherds:

- Average premium: $40-55/month

- Generally healthy working breeds

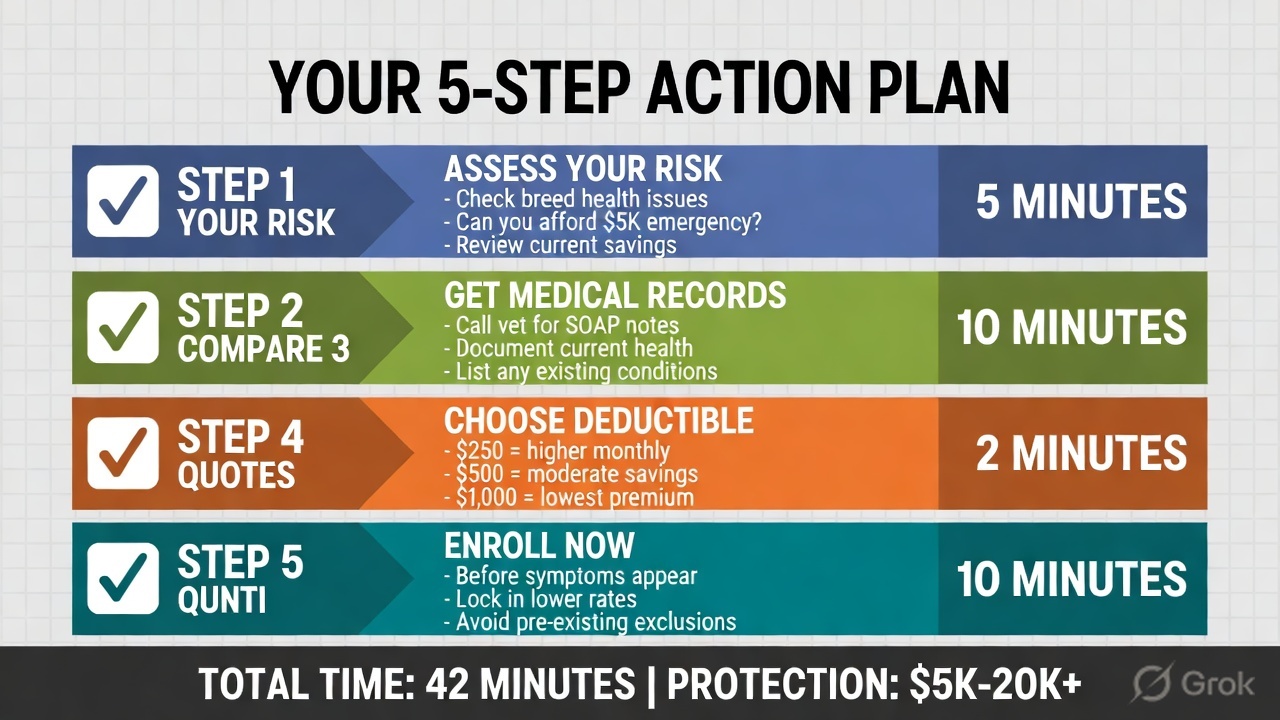

The Claims Roadmap: How to Get Paid

Step-by-Step Process:

1. Visit Any Licensed Vet

- Most U.S. policies work at any vet in the U.S. or Canada

- No network restrictions (unlike human health insurance)

- Specialists and emergency clinics are all covered

2. Pay Upfront (Most Providers)

- Unless using Trupanion (direct-to-vet payment)

- Use a credit card, CareCredit, or emergency savings

- Get an itemized invoice before leaving

3. Collect “SOAP” Notes

- Subjective, Objective, Assessment, Plan

- These detailed clinical notes prove the condition timeline

- Critical for avoiding “pre-existing” denials

- Ask vet: “Can I get the full SOAP notes for insurance?”

4. Submit via App (Digital)

- Take a photo of the itemized invoice

- Upload medical records/SOAP notes

- Most providers have mobile apps (Lemonade, Spot, Pumpkin, ASPCA)

- Some still accept email or fax (MetLife)

5. Wait for Processing

- Lemonade: Seconds to 24 hours (AI instant approval)

- Spot: 3.3 days average

- Pumpkin: 2-5 days (urgent pay: 15 minutes)

- ASPCA/MetLife: 5-10 days

6. Reimbursement

- Direct deposit to bank account

- Zelle or PayPal (some providers)

- Check (slowest option)

Pro tip: Submit claim from vet parking lot while details are fresh. The faster you submit, the faster you get paid.

Consumer Red Flags to Watch For

As premiums rise, some lower-tier insurers use “fine print” to deny claims. Be vigilant for:

🚩 Red Flag 1: Bilateral Exclusions

What it is: If your dog has a knee injury on the LEFT leg before enrollment, some insurers exclude the RIGHT leg forever—even though it was never injured.

Why it’s unfair: Treats future injuries as “related” when they’re not.

Who does this: Lower-tier providers, especially cheap plans.

How to avoid: Ask specifically: “Do you have bilateral exclusion clauses?” Choose providers who don’t (ASPCA, MetLife, Spot).

🚩 Red Flag 2: Vague “Symptoms” Clauses

What it is: Plans that deny claims for any condition that “showed signs” before the 14-day waiting period ended.

Example: Dog limps once, 10 days after enrollment. At day 20, diagnosed with a torn ACL. Denied because “limp was a symptom during the waiting period.”

Why it’s unfair: Minor symptoms don’t mean the condition existed.

How to avoid: Get a pre-enrollment vet exam. Document that the pet is healthy at sign-up.

Recommendation: Minimum $10,000 annual limit. Better: $20K+. Best: Unlimited (Spot, MetLife, ASPCA).

🚩 Red Flag 3: Rapid Premium Increases

What it is: Premiums jumping 25-30% at renewal (vs industry average 15-20%)

Example: Year 1: $40/month. Year 2: $52/month (+30%). Year 3: $67/month (+29%).

Why it’s a problem: Becomes unaffordable, forcing you to drop coverage when your pet needs it most.

How to avoid: Check reviews for “premium increase complaints.” Lemonade and Spot have the most stable increases historically.

Read full breakdown of 2026 premium increases →

Alternatives to Traditional Insurance

For the 3 in 4 Americans without insurance, these options provide a partial safety net:

Option 1: Pet Medical Savings Account (MSA)

How it works:

- Open high-yield savings account (4-5% APY)

- Automatic transfer: $50-100/month

- Build to $3,000-5,000 emergency fund

Pros: ✅ You keep the money if the pet stays healthy

✅ No premiums, deductibles, or claim denials

✅ Full control over funds

Cons: ❌ Takes 2-4 years to build an adequate fund

❌ Vulnerable during the building phase

❌ One emergency wipes out savings, start over

Best for: Disciplined savers, healthy young pets, stable income

Option 2: CareCredit Healthcare Financing

How it works:

- Healthcare credit card accepted at 26,000+ vets

- 0% interest promotional periods (6-24 months)

- Apply in advance (approval takes 5 minutes)

Pros: ✅ Immediate access to funds for emergencies

✅ 0% interest if paid off during promo period

✅ Can use for human healthcare too

Cons: ❌ Requires credit approval

❌ Retroactive 26.99% interest if not paid in full by promo end

❌ Easy to fall into a debt trap

Best for: Emergency backup with discipline to pay off quickly

Warning: If you can’t pay off $5,000 in 18 months, don’t rely on this.

Option 3: Buy Now, Pay Later (BNPL)

Providers:

- Scratchpay: Veterinary-specific financing

- Cherry: 0% financing for healthcare

- PayPal Credit: Accepted at some vets

How it works:

- Split $3,000 bill into $250/month for 12 months

- Approval based on soft credit check

- Interest varies (0-15% depending on credit)

Pros: ✅ Easier approval than credit cards

✅ More flexible than saving up front

Cons: ❌ Still debt

❌ Interest adds up

❌ Not all vets accept

Option 4: Charity Grants & Assistance

Organizations:

- RedRover Relief: (916) 429-2457 – Emergency grants up to $200-300

- The Pet Fund: (916) 443-6482 – Non-routine care up to $500

- Brown Dog Foundation: Cancer treatment assistance

- Frankie’s Friends: Life-saving care grants

- Shakespeare Animal Fund: California-based, up to $1,000

How it works:

- Apply online with vet estimate

- Proof of financial need required

- Funds paid directly to the vet

Pros: ✅ Free money (no repayment)

✅ Can cover a significant portion

Cons: ❌ Limited funds (not guaranteed)

❌ Long wait times (days to weeks)

❌ Income requirements

❌ Not for routine care

Best for: Low-income families, life-threatening emergencies

Option 5: Hybrid Approach (Smart Strategy)

Combination:

- Accident-only insurance ($10-20/month) – covers catastrophic accidents

- Savings fund ($50/month) – builds to $3,000 for illnesses

- CareCredit backup – emergency bridge if needed

Cost: $60-70/month total (similar to full insurance)

Coverage: ✅ Accidents covered immediately (hit by a car, broken bones, poisoning)

✅ Illnesses covered from savings (once built up)

✅ CareCredit if savings not yet built or major emergency

Best for: Budget-conscious owners who want some protection while building savings

Frequently Asked Questions

Q: Is pet insurance worth it for an indoor cat?

A: Yes. Indoor cats are prone to high-cost chronic issues:

- Hyperthyroidism: $1,000-2,000/year treatment

- Diabetes: $1,500-3,000/year (insulin, monitoring)

- Urinary blockages: $2,000-4,000 per incident (life-threatening)

- Kidney disease: $2,000-5,000/year management

Indoor doesn’t mean risk-free. It means different risks (chronic vs trauma).

Q: Why did my premium go up 20% if I never filed a claim?

A: Premiums are “pooled” across all policyholders. They rise because:

- Your pet aged (higher risk category)

- Veterinary costs increased 11% in your area

- Other customers filed expensive claims (everyone shares the cost)

- The insurance company needs to maintain reserves

Your individual claim history doesn’t matter—it’s about the group risk pool.

Read full explanation of 2026 premium increases →

Q: Can I get insurance if my pet is already sick?

A: Yes, you CAN enroll, but:

- ❌ The specific diagnosed illness = pre-existing = NOT covered

- ✅ New, unrelated accidents or illnesses = covered after waiting period

Example: Dog has diabetes (pre-existing). Enrollment allowed. Diabetes treatment is not covered. But if the dog breaks a leg 3 months later, that’s covered.

Strategy: Enroll while the pet is healthy to avoid exclusions.

Q: What is the most common reason for a denied claim?

A: Top 3 denial reasons:

Pre-existing conditions (60% of denials)

- Condition existed before enrollment

- Symptoms appeared during the waiting period

Claims during waiting period (25% of denials)

- Filed before the 14-day illness wait ended

- Many people don’t understand this

Incomplete documentation (10% of denials)

- Missing itemized invoice

- No medical records/SOAP notes

- Vet didn’t specify diagnosis codes

How to avoid: Get a pre-enrollment vet exam, wait out all waiting periods, and submit complete documentation.

Q: Does insurance cover vaccines and grooming?

A: Standard accident/illness plans do NOT cover:

- Routine vaccines

- Annual wellness exams

- Dental cleanings (unless illness-related)

- Grooming

- Flea/tick prevention

- Spay/neuter

You must add a “Wellness” or “Preventive Care” rider (extra $15-35/month) to cover these.

Riders available:

- ASPCA: Preventive Care package ($20/month, covers $450/year)

- Spot: Gold Plan wellness ($25/month)

- Pumpkin: Preventive Essentials ($30/month, covers $500/year)

Worth it? Usually not. Most riders reimburse $450-500/year but cost $240-360/year. You’re paying $300 to get $450 back = $150 net benefit. Better to budget $40/month for routine care yourself.

Q: Can I switch providers mid-year without losing coverage?

A: You can switch anytime, BUT:

What transfers:

- ✅ Your pet’s age/breed history

- ✅ Your knowledge of the claim process

What DOESN’T transfer:

- ❌ Any conditions treated at the old provider become pre-existing at the new provider

- ❌ Waiting periods restart (14 days illness, 6 months orthopedic)

- ❌ Annual deductible restarts

Best timing: Switch at the annual renewal date, when the pet is healthy with no active conditions.

Exception: If your current provider raised premiums 25%+, switching might be worth restarting waiting periods.

Q: What happens if I miss a payment?

A: Most providers have a 30-day grace period:

- Days 1-15: Reminder emails

- Days 16-30: Coverage suspended, urgent payment request

- Day 31: Policy canceled

If canceled:

- ❌ All coverage lost

- ❌ Any conditions developed during policy = pre-existing if you re-enroll

- ❌ Can’t just restart where you left off

To avoid: Set up auto-pay. One missed payment can cost you everything.

Final Verdict and Next Steps

The 20% premium jump is a significant challenge, but the cost of not having coverage in 2026 is far higher. With emergency surgeries exceeding $5,000-10,000 and cancer treatment reaching $15,000-20,000, being among the 1 in 4 insured Americans isn’t a luxury—it’s financial protection.

Questions about choosing the right provider?

Email: fursurely100@gmail.com

We’ll help you compare quotes and choose the best fit for your pet and budget.

Share this guide: Every pet owner should understand their options.

📧 Email | 💬 Facebook | 🐦 Twitter | 🔖 Bookmark

Related Reading:

- Why Pet Insurance Increased 20% in 2026 (And How to Fight Back) →

- Fursure Lost Its Debit Card — 5 Alternatives with Direct Payment →

- Emergency Vet Costs Up 18% in 2026 — How to Prepare →

About FurSurely: We make pet insurance simple. Only 1 in 4 Americans have coverage, and we’re here to help you understand whether you should join them—or save your money. Where Fur Meets Sure.

Last Updated: February 26, 2026