Pet Insurance Claims in 6 Minutes: What AI Means for U.S. Owners (2026)

Meta Description: Pet insurance now pays in 6 minutes vs 2-4 weeks. See which U.S. providers offer instant claims in 2026 + how to choose the right one for your pet.

Table of Contents

- The Sock Story: When Every Second Counts

- How 6-Minute Claims Actually Work

- Real Story: From Crisis to Relief in 15 Minutes

- Provider Speed Comparison

- Which Provider Should You Choose?

- What to Watch Out For

- Can’t Afford Insurance Right Now?

- What You Should Do This Week

- Your Questions Answered

The Sock Story: When Every Second Counts

Picture this moment:

It’s 9 PM on a Tuesday. Your golden retriever, Max, just threw up a sock—one he apparently swallowed three days ago. He’s whimpering, won’t eat, and his belly feels hard as a rock.

You rush to the emergency vet. They take one X-ray and deliver the news: “He needs surgery within the next few hours, or this could turn life-threatening. The cost will be around $4,500.”

Your heart drops. Your credit card is nearly maxed out from holiday spending. You have pet insurance, but the thought of fronting $4,500 and then waiting weeks for reimbursement makes you feel sick.

Then your phone buzzes: “Claim approved. $3,825 deposited to your account.”

Six minutes. That’s all it took.

This isn’t fiction anymore. As of February 2026, this is the new standard in Europe—and it’s officially arrived in America. While only 4% of U.S. dog owners and 1% of cat owners currently have pet insurance (that’s just 3.8 million pets out of 94 million households), the main barrier has always been the same: slow, complicated claims that leave you stuck with debt for weeks.

That barrier just collapsed.

How 6-Minute Claims Actually Work

Remember filing insurance claims five years ago? It felt like a part-time job:

The Old Way (and unfortunately, still common):

- Pay the vet $4,000 on your credit card

- Request itemized invoices from the clinic

- Fill out claim forms (front and back)

- Mail, fax, or scan everything to the insurance company

- Wait 2-4 weeks while someone manually reviews your paperwork

- Hope nothing gets denied

- Maybe get your money back

The New Way (AI-Powered Claims):

- Pay the vet $4,000

- Open your phone app while still in the parking lot

- Take a photo of the invoice

- Hit “Submit.”

- Advanced AI reads the bill, verifies your policy coverage, checks for fraud, and approves payment

- Money hits your account in 6-15 minutes

No forms. No scanning. No waiting. No stress about whether you can pay rent next month.

The Technology Behind It

You don’t need to understand the technical details, but here’s the simple version: Modern AI can now “read” veterinary invoices—even handwritten ones—with 96-98% accuracy (that’s better than humans). It cross-checks your pet’s medical history, verifies your policy details, spots potential fraud, and makes a decision faster than you can finish your coffee.

The company that set this record? A Swedish insurer called Lassie. They just raised $75 million and process 60% of their claims in under six minutes.

And now, American companies are racing to catch up.

Real Story: From Crisis to Relief in 15 Minutes

Sarah M., Austin, Texas | Lemonade Customer

“It was 8 PM on a Tuesday. My beagle, Charlie, got into a bag of dark chocolate while I was making dinner. I knew chocolate was toxic, so I rushed him to the emergency vet immediately.

They induced vomiting and monitored him for three hours. The bill came to $2,200. I submitted the claim through Lemonade’s app at 10:15 PM, literally from my car in the parking lot before I drove home.

By 10:30 PM—15 minutes later—I got the notification: ‘Claim approved. $1,980 deposited.’ I actually pulled over to make sure it was real.

I’ve told every dog owner I know about this. The old company I had would have taken two weeks and asked me for three different forms. This felt like magic.”

Sarah’s experience isn’t rare anymore. It’s becoming the standard.

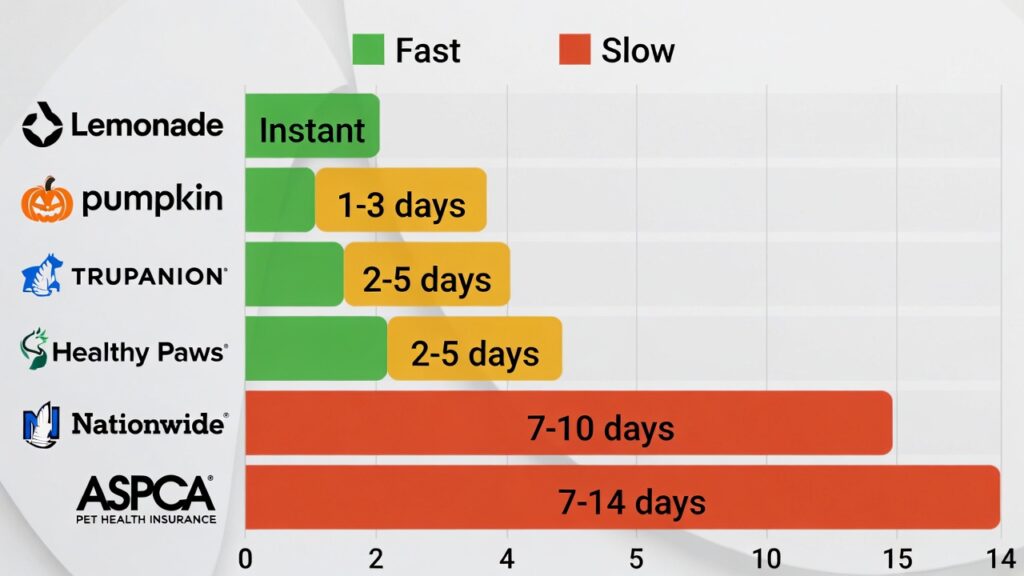

U.S. Provider Speed Comparison (February 2026)

Here’s how the major U.S. providers stack up on claim speed:

| Provider | How Fast? | Best For | Monthly Cost (Dog) | Our Rating |

|---|---|---|---|---|

| Pumpkin | 15 minutes (urgent pay) | Emergency funds needed | $68 | ⭐⭐⭐⭐⭐ |

| Lemonade | Instant (50% of claims) | Tech-savvy, budget-conscious | $31 | ⭐⭐⭐⭐⭐ |

| Trupanion | Pays vet directly | Never want to front money | $50+ | ⭐⭐⭐⭐ |

| Healthy Paws | 2 days average | Traditional, reliable option | $45 | ⭐⭐⭐⭐ |

| Pets Best | 3-5 days | USAA members, customizable | $40+ | ⭐⭐⭐ |

| Nationwide | 5-10 days | Existing customers, birds/exotics | $45+ | ⭐⭐⭐ |

| ASPCA | 7-14 days | Non-profit option | $50+ | ⭐⭐ |

💡 Our Top Picks:

Best for Emergencies: Pumpkin

If you can’t afford to front $1,000+, their “PumpkinNow” urgent pay gets you reimbursed in 15 minutes for major bills.

Best for Budget: Lemonade

At $31/month for dogs, they’re the cheapest option with instant claim approval for 50% of submissions.

Best for Zero Out-of-Pocket: Trupanion

They pay your vet directly at checkout using your pet’s microchip. You literally never touch the money.

Which Provider Should You Choose?

Stop staring at comparison charts. Here’s the simple decision tree:

Do you have $1,000+ in emergency savings?

YES → Go with Lemonade ($31/month, instant claims)

- Cheapest premium

- Fast claims for routine issues

- You can handle fronting money for 15-30 minutes

NO → Go with Trupanion or Pumpkin

- Trupanion: Pays vet directly (you front $0)

- Pumpkin: 15-minute urgent pay for big bills

Is your dog a “high-risk” breed?

Bulldogs, German Shepherds, Golden Retrievers, Rottweilers, and Great Danes all fall into this category due to genetic health issues.

Go with Healthy Paws or Embrace

- No lifetime caps (critical for chronic conditions)

- Covers hereditary conditions

- Diminishing deductibles reward healthy years

Do you have a cat?

Cats are generally cheaper to insure ($18-30/month). Almost any provider works well, but:

Best value: Lemonade ($18/month)

Most comprehensive: Healthy Paws (no caps)

Is your pet over 8 years old?

Most providers won’t insure new pets over 14, and premiums jump significantly after age 8.

Best for seniors: Embrace (diminishing deductible) or Pets Best (customizable)

Avoid: Accident-only plans (seniors need illness coverage)

What to Watch Out For: Breed-Specific Risks

Modern AI uses massive databases to predict which breeds cost more to insure. This isn’t discrimination—it’s mathematics based on millions of vet visits.

Here’s what owners of “expensive breeds” need to know:

German Shepherds

- Common issue: Hip dysplasia ($1,500-$6,000 per joint)

- AI flag: Genetic predisposition

- Your move: Enroll before age 2, choose plans covering hereditary conditions

Bulldogs (English & French)

- Common issue: Breathing problems, skin infections

- Highest claim on record: $60,215 (pneumonia complications)

- Your move: Accept higher premiums ($80-120/month), never skip coverage

Golden Retrievers

- Common issue: Cancer (60% develop it), hip dysplasia

- Average cancer treatment: $5,000-$15,000

- Your move: Choose plans with no lifetime caps (Healthy Paws, Embrace)

Labrador Retrievers

- Common issue: Joint problems, obesity-related conditions

- Average ACL surgery: $3,500-$5,000

- Your move: Start coverage young, maintain a healthy weight

The Good News

Even with higher premiums, insurance still makes financial sense. A $90/month premium ($1,080/year) beats a single $15,000 cancer treatment.

The Caution

Always choose providers that offer: ✅ Human review for denied claims

✅ Clear explanations for denials (not just “computer says no”)

✅ An appeals process

✅ Coverage for hereditary/congenital conditions

Red flags: ❌ “Pre-existing condition” definitions that are too broad

❌ Bilateral exclusions (if one knee tears, the other is excluded)

❌ No explanation for instant denials

Can’t Afford Insurance Right Now? Bridge the Gap With These

Look, we get it. Not everyone can afford $40-70/month for pet insurance, especially with inflation hitting groceries, rent, and everything else.

Here are two options that can help until you’re ready for full coverage:

1. Accident-Only Insurance ($10-20/month)

Covers: ✅ Emergency surgeries (foreign objects, broken bones)

✅ Poisoning incidents

✅ Hit by a car

✅ Snake bites, bee stings

Doesn’t cover: ❌ Cancer

❌ Infections

❌ Chronic conditions

❌ Routine care

Best for: Young, healthy pets; tight budgets

Providers: Lemonade ($10-15/month), Figo ($15-20/month)

2. Banfield Wellness Plans ($35-65/month)

These aren’t insurance—they’re prepaid care packages.

Includes: ✅ Unlimited office visits

✅ Vaccines

✅ Annual exams

✅ Teeth cleaning

✅ Fecal exams

Doesn’t include: ❌ Emergency care

❌ Surgery

❌ Hospitalization

❌ Specialist visits

Best for: Routine care budgeting; not accident protection

Savings: About 30% on preventive care

3. CareCredit Healthcare Card

Not insurance—it’s a credit card specifically for medical expenses (human and pet).

Benefits:

- 0% interest for 6-18 months (depending on the bill size)

- Covers vet bills, medications, and even pet dental work

- Accepted at most veterinary practices

Best for: Covering high deductibles or unexpected bills while waiting for insurance reimbursement

Warning: After the promotional period, interest rates jump to 26-30%. Pay it off fast.

Our Honest Recommendation

Even if you start with just accident-only coverage at $15/month, it’s infinitely better than nothing. The worst financial decisions happen at 9 PM in an emergency vet’s office when you’re emotional and don’t have options.

What You Should Do This Week

Don’t bookmark this and forget about it. Take 20 minutes right now to protect your pet (and your wallet).

Step 1: Check Your Current Speed (5 minutes)

If you already have insurance: Call your provider and ask: “How long does it typically take from claim submission to money in my account?”

- If they say 7+ days: You’re overpaying for slow service. Compare alternatives.

- If they say “it depends”: That means slow. Get a real answer.

- If they say “24-48 hours or less”: You’re in good shape, but still check premiums.

Step 2: Compare Your Rate (2 minutes)

Check real-time quotes based on your pet’s breed and age using a pet insurance comparison tool. Many owners discover they’re paying 20–40% more than necessary.

Key question: Are you getting the fastest claim speed for your premium price?

Step 3: Enroll NOW If You Don’t Have Coverage (5 minutes)

This is critical: Once your pet shows symptoms of anything—limping, coughing, skin issues—it becomes a “pre-existing condition” and will NEVER be covered.

The window is now. While your pet is healthy.

- Puppies/kittens under 1 year: Cheapest rates, no health history

- Adults 1-7 years: Still affordable, lock in now

- Seniors 8+ years: Rates jump, but still worth it (chronic conditions cost more)

Don’t wait for: ❌ “After the holidays.”

❌ “When I have more money.”

❌ “When they’re older and need it more.”

By the time they “need it more,” it’s too late. Pre-existing conditions = no coverage.

Your Questions Answered

Q: Is Lassie (the 6-minute Swedish company) available in the U.S.?

A: Not yet. Lassie currently operates in Sweden, Germany, and France. However, U.S. providers like Lemonade and Pumpkin already offer comparable speeds (instant to 15 minutes). See our comparison table above.

Q: Why was my claim denied instantly by AI?

A: The most common reasons:

- Pre-existing condition flagged in your pet’s medical history

- Waiting period hasn’t passed (usually 14 days for illnesses, 2 days for accidents)

- Breed exclusion for that specific condition

- Policy limit already reached for the year

You’re right: You can ALWAYS appeal and request a human reviewer. Most denials have explanations; if yours doesn’t, that’s a red flag about your provider.

Q: Does insurance cover routine dental cleanings?

A: Usually no. Standard plans cover:

- ✅ Broken teeth from accidents (hit by a car, chewing something hard)

- ✅ Tooth extractions due to disease

- ❌ Routine cleanings and preventive dental care

For routine cleanings, you need a “Wellness” add-on (extra $10-25/month) or a Banfield plan.

Q: How much do premiums increase as my pet ages?

A: On average, dog insurance premiums increase by $26.50/year as your pet ages. For example:

- Age 2: $35/month

- Age 5: $45/month

- Age 8: $60/month

- Age 10: $85/month

Pro tip: Some providers (like Embrace) offer diminishing deductibles that reward you for claim-free years, which can offset age-related increases.

Q: Can I use pet insurance at any vet?

A: Yes! Unlike human health insurance, pet insurance has no “networks.” You can use any licensed veterinarian, specialist, or emergency clinic in the U.S. (Some providers even cover international care if you’re traveling.)

Q: What happens if I cancel and then re-enroll later?

A: Any health issues that occurred during the gap become pre-existing conditions and won’t be covered. This is why you should never cancel during treatment or if your pet has any ongoing issues.

Example: Your dog tears his ACL in year 2. You cancel insurance in year 3. You re-enroll in year 4. That knee (and possibly both knees) is now excluded forever.

Q: Is pet insurance tax-deductible?

A: For most pet owners, no. HOWEVER, it may be deductible if:

- Your pet is a certified service animal for a disability

- Your pet is used for business (farm animals, guard dogs for businesses)

Consult a tax professional for your specific situation.

Q: Do I need insurance if I have $10,000 in savings?

A: This is personal, but consider: The average cancer treatment is $5,000-$15,000. Hip surgery is $4,000-$6,000. If your pet has both (not uncommon for Golden Retrievers), that’s $10,000-$20,000.

Insurance costs $500-$800/year. Even with savings, it’s usually worth it for peace of mind and protecting your nest egg.

The Bottom Line: Speed is the New Standard

Five years ago, waiting 2-3 weeks for pet insurance reimbursement was normal. Today, it’s obsolete.

If your current provider can’t process claims in 48 hours or less, you’re paying for outdated service. The technology exists. The competition is fierce. You have options.

The new standard is:

- ⚡ Instant to 15-minute approval for routine claims

- 📱 Mobile-first submission (no paperwork)

- 💳 Direct deposit, not mailed checks

- 🤖 AI accuracy that beats human review

- 👨⚕️ Human oversight for complex cases

What you should demand from your provider:

- Clear timeline for reimbursement

- Mobile app with photo submission

- Explanation for any denials

- Human review option for disputes

- Competitive pricing for fast service

The companies that can’t deliver this will be gone in 3-5 years. The ones that can are growing 30-40% annually.

Choose wisely. Your future self—and your pet—will thank you.

Fursure Acquired by Physicians Mutual: What Pet Owners Need to Know (2026 Update)