Pet Insurance Premiums Jumped 15% in 2026: What U.S. Pet Owners Need to Know Now

Last Updated: February 16, 2026

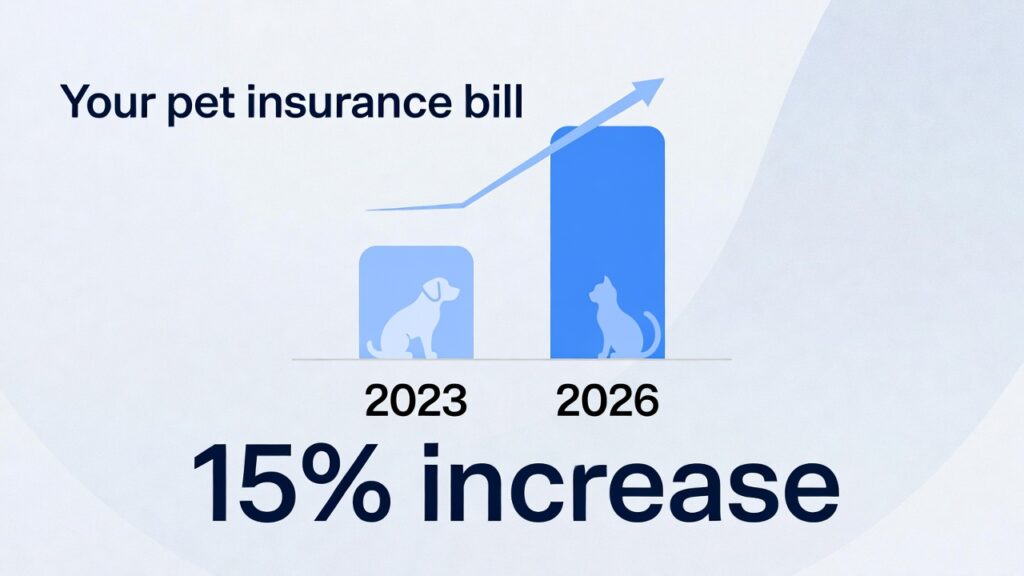

Pet insurance premiums rose an average of 15% in 2026, and for millions of American pet owners, the increase felt sudden.

But it wasn’t random.

Behind the jump is a bigger shift happening across U.S. veterinary medicine — rising surgical costs, advanced diagnostics becoming “standard care,” and consolidation of clinics under private equity groups.

The result?

Pet insurance isn’t just growing — it’s becoming more expensive and more essential at the same time.

Here’s what’s really happening, what it means for your wallet, and how to protect yourself before the next emergency.

The 2026 Pet Insurance Market: Growth With Pressure

The North American pet insurance market has now surpassed $5.2 billion in written premiums, yet only about 4% of U.S. pets are insured.

That means 96% of dogs and cats are financially exposed to:

$3,000 emergency surgeries

$5,000 hospitalization bills

$10,000 cancer treatments

Meanwhile, veterinary costs are rising faster than general inflation. Emergency visits that averaged $1,200 just a few years ago now frequently exceed $1,800–$2,500.

Insurance companies are adjusting premiums to keep up.

The 15% increase isn’t a random markup. It reflects structural changes in veterinary medicine.

Why Premiums Jumped 15% in 2026

1. Clinical Inflation (Not Just Regular Inflation)

Veterinary care today includes:

CT scans

MRIs

Targeted oncology

Advanced orthopedic surgery

24/7 ICU hospitalization

These services didn’t exist at scale 15 years ago. Now they’re considered normal.

An ACL surgery that once cost $2,500 can now exceed $6,000 in urban areas.

Insurance premiums adjust accordingly.

2. Private Equity and Clinic Consolidation

Independent veterinary practices are increasingly being acquired by corporate groups.

This leads to:

Standardized diagnostic protocols

More bundled testing

Higher base procedure pricing

While care quality often improves, claim sizes rise — and insurers price that risk into future premiums.

3. Aging Pet Population

More pets are living longer.

A 2-year-old dog might cost $40/month to insure.

That same dog at age 9 may cost $95/month.

Insurance pricing reflects risk, and risk increases with age.

If you’re new to how coverage actually works, read our complete breakdown of how pet insurance works in the U.S. before comparing plans.

What Pet Insurance Actually Covers in 2026

Understanding policy types matters more than ever.

Accident-Only Coverage

Average cost:

Dogs: ~$17/month

Cats: ~$10/month

Covers:

Broken bones

Car accidents

Toxic ingestion

Does NOT cover:

Cancer

Infections

Chronic disease

Best for: Budget-conscious owners wanting catastrophic protection only.

Accident + Illness (Comprehensive Plans)

Covers:

Cancer

Diabetes

Kidney disease

Infections

Hereditary conditions

This is what most insured pet owners carry.

It’s also the category most affected by the 15% increase.

Wellness Add-Ons

Covers:

Vaccines

Annual exams

Flea/tick meds

Important note: Wellness plans are budgeting tools — not financial protection against emergencies.

Always calculate if the rider costs more than the services it covers.

Not sure whether insurance still makes sense after this price hike? See our detailed analysis on whether pet insurance is still worth it in 2026.

Leading Providers in Early 2026

While pricing fluctuates by ZIP code and breed, here are standout providers based on coverage structure and consumer experience:

ASPCA – Broadest Coverage Scope

Covers dental illness and behavioral therapy

Includes alternative therapies

Strong option for comprehensive protection

MetLife – Best for Multi-Pet Homes

Shared deductible across multiple pets

Zero-day accident waiting period

Spot – High-Limit Coverage + Telehealth

Unlimited annual payout options

24/7 vet hotline

Pumpkin – High Reimbursement Simplicity

Standard 90% reimbursement

No upper age enrollment limit

Each provider structures risk differently. The “cheapest” policy isn’t always the best long-term choice.

How Pricing Really Works (The Actuarial Logic)

Your premium is based on:

1. Geography

A dog in California may cost $54/month.

The same dog in Louisiana may cost $34/month.

Veterinary labor and facility costs drive this difference.

2. Age

Premiums rise as pets age.

Example:

Age 2: $39/month

Age 8: $98/month. If you can’t sustain rising premiums later, consider adjusting deductibles early.

3. Deductible & Reimbursement

Lower monthly premium = higher out-of-pocket risk.

Common settings:

$250 deductible / 90% reimbursement

$500 deductible / 80% reimbursement

$1,000 deductible / 70% reimbursement

Choosing a $1,000 deductible can significantly reduce your monthly cost while still protecting you from a $15,000 emergency.

Breed Risk: The Financial Reality

Certain breeds carry a higher lifetime risk.

| Breed | Avg Monthly Premium | Primary Risk |

|---|---|---|

| Bulldog | ~$87 | Respiratory, orthopedic |

| Golden Retriever | ~$57 | Cancer |

| German Shepherd | ~$53 | Hip dysplasia |

| Dachshund | ~$64 | Spinal disease |

| Maine Coon | ~$52 | Heart disease |

If you own a high-risk breed, unlimited or high-limit coverage is strongly recommended.

Real 2026 Claim Math

Scenario 1: Toxic Ingestion (Dog)

Vet bill: $3,500

Policy: $250 deductible / 90% reimbursement

Calculation:

$3,500 – $250 = $3,250

$3,250 × 90% = $2,925 reimbursed

Your cost: $575

Scenario 2: Urinary Blockage (Cat)

Vet bill: $3,000

Policy: $500 deductible / 80% reimbursement

Calculation:

$3,000 – $500 = $2,500

$2,500 × 80% = $2,000 reimbursed

Your cost: $1,000

Without insurance? Full $3,000 at checkout.

Red Flags to Watch in 2026

With rising premiums, some insurers quietly tighten rules.

Watch for:

❗ Vague pre-existing condition wording

❗ Bilateral exclusions (one ACL tear excludes the other)

❗ Low annual payout caps ($5,000 is risky)

❗ Post-claim premium spikes

❗ Limited “direct pay” networks

Always read the policy language — not just the marketing page.

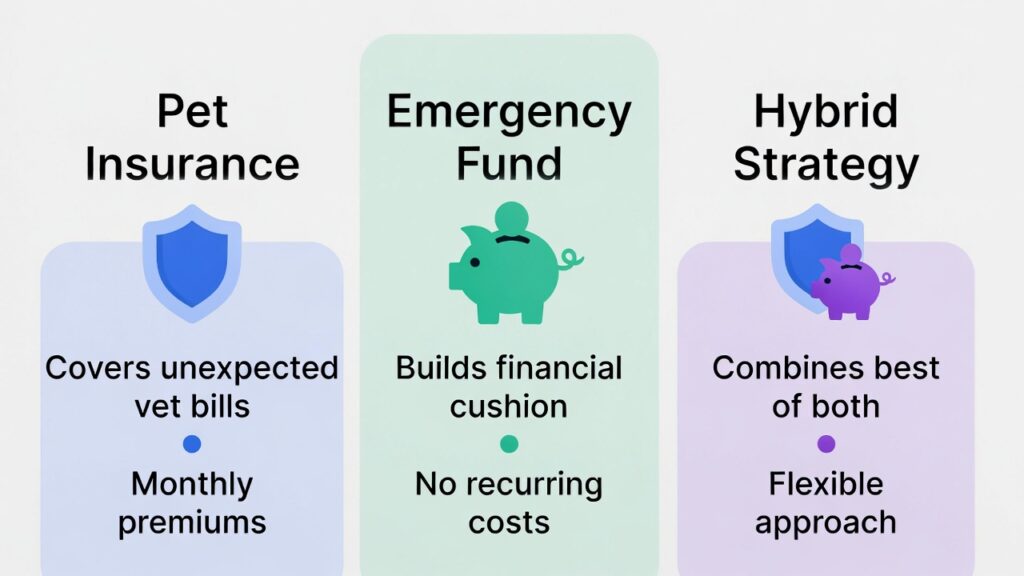

Alternatives to Insurance

Insurance isn’t the only path, but it is the only risk-transfer mechanism.

1. Dedicated Pet Emergency Fund

Pros:

Full control of money

No exclusions

Cons:

A $10,000 surgery can happen before you save that much

Target savings: $5,000–$10,000

2. CareCredit / Payment Plans

Often 0% interest for 6–18 months.

Risk: Retroactive interest if unpaid on time.

3. Charity Support

Organizations like:

Banfield Foundation

Brown Dog Foundation

Frankie’s Friends

These are last-resort safety nets, not primary plans.

The Bigger Picture

The 15% premium increase isn’t about greed. It reflects:

Advanced veterinary technology

Rising labor costs

Corporate consolidation

Higher claim severity

But here’s the uncomfortable truth:

Veterinary costs are unlikely to fall.

Which means financial preparation is no longer optional.

Action Steps for 2026

Compare your current premium to at least two competitors.

Request full medical records (establish documentation history).

Build a $1,500 deductible buffer fund.

Consider raising your deductible if premiums feel too high.

Enroll early — once diagnosed, conditions become pre-existing.

Frequently Asked Questions

Q: Why did my premium increase if I never filed a claim?

A: Risk pools adjust annually based on age and local vet inflation — not just personal usage.

Q: Is insurance worth it for young pets?

A: Yes. That’s when premiums are lowest, and coverage is cleanest.

Q: What’s the most common claim denial?

A: Pre-existing conditions and issues occurring during the 14-day waiting period.

Final Thought

Pet ownership in 2026 carries higher financial responsibility than ever before.

Insurance may cost $30–$50 per month.

An emergency may cost $6,200 at 2 AM.

Preparation feels expensive — until you compare it to panic.

Questions? fursurely100@gmail.com |

Share this: Every pet owner should know this before an emergency.

📧 Email | 💬 Facebook | 🐦 Twitter

The cost of preparation: $30-50/month or 20 minutes.

The cost of being unprepared: $6,200 at 2 AM.

Choose wisely.

About FurSurely: We help U.S. pet owners understand real veterinary costs and find affordable protection. We work for you, not insurance companies.

Last Updated: February 16, 2026