Emergency Vet Bills Are Up 18% in 2026 — Here’s How Smart Pet Owners Are Protecting Themselves.

Meta Description: Emergency vet costs jumped 18% in 2026, with visits averaging $800 to $1,500. Learn the real costs, why prices are rising, and 5 proven strategies to avoid financial disaster.

Last Updated: February 16, 2026

Last month, Jessica rushed her Labrador to the emergency vet at 11 PM. Max had eaten something—nobody knows what—and was vomiting non-stop.

The diagnosis? Intestinal blockage requiring immediate surgery.

The estimate? $6,200.

Jessica had $800 in her checking account. She stood in that fluorescent-lit waiting room, trying to decide if she could afford to save her dog’s life.

She’s not alone. Emergency vet visits have jumped 18% in cost since last year, and the average bill now sits between $800 and $1,500—before any actual treatment begins.

But here’s what most pet owners don’t know: The people who handle these emergencies without financial panic aren’t necessarily wealthier. They just prepared differently.

If you’re unsure how reimbursement actually works, read our detailed guide on how pet insurance works in 2026.

What Emergency Vets Actually Cost in 2026

Here’s what “average” really means when your pet needs emergency care:

Just Walking Through the Door

- Emergency exam fee: $150-$250

- After-hours surcharge: $75-$150

- Before they even touch your pet: $225-$400

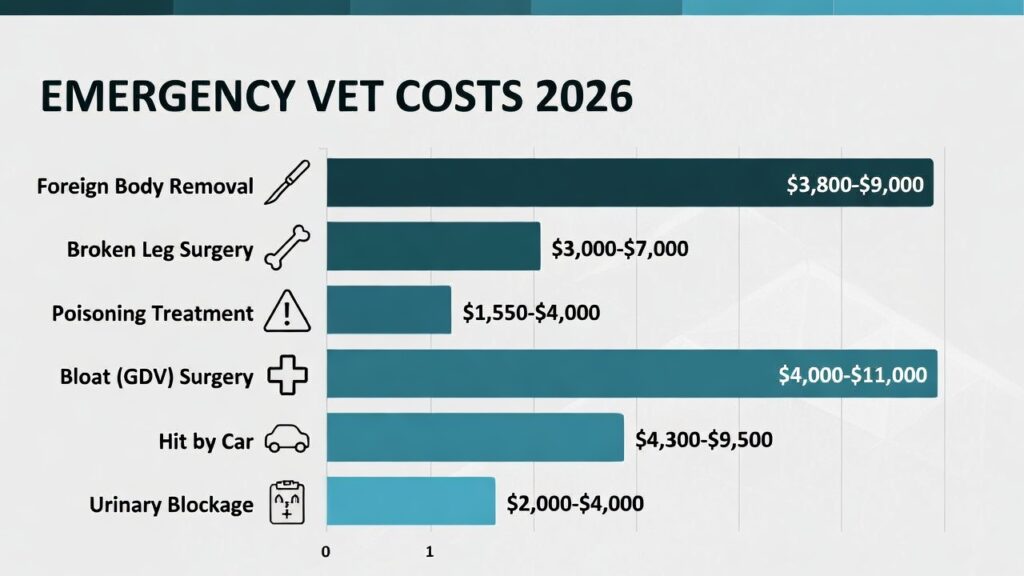

Common Emergency Costs (Full Treatment)

| Emergency | Total Cost Range |

|---|---|

| Foreign body removal (ate something) | $3,800-$9,000 |

| Broken leg with surgery | $3,000-$7,000 |

| Poisoning treatment | $1,550-$4,000 |

| Bloat (GDV) emergency surgery | $4,000-$11,000 |

| Hit by a car (moderate injuries) | $4,300-$9,500 |

| Urinary blockage (cats) | $2,000-$4,000 |

These aren’t scare tactics. These are actual numbers from U.S. emergency veterinary hospitals in February 2026.

Why Costs Jumped 18% (And Why They’ll Keep Rising)

1. Corporate Consolidation Changed Everything

Since 2017, nearly 1 in 3 veterinary practices have been acquired by corporations backed by private equity. When local vets get bought, prices typically increase immediately.

Why? Corporations have higher debt payments, larger management costs, and profit expectations of 20-30% annual returns. Your emergency bill now includes paying off billion-dollar acquisition loans.

2. Veterinarian Shortage = Higher Salaries

Emergency vets are scarce. To compete for talent, clinics are offering:

- $150K-$250K starting salaries (up from $80K-$120K five years ago)

- $20K-$50K signing bonuses

- Full relocation expenses

Those costs get passed directly to you.

3. Advanced Equipment Is Now Standard

Modern emergency vets need digital X-rays ($50K-$100K), ultrasound machines ($40K-$80K), and advanced surgical suites ($200K+). Equipment that barely existed in emergency clinics 10 years ago is now mandatory—and expensive.

4. 24/7 Staffing Costs Are Brutal

Unlike regular vets (8 AM – 6 PM), emergency clinics run around the clock. That means night shift premiums (1.5-2x pay), holiday staffing (triple pay), and fully staffed weekends.

Plus: Veterinary medications (+12%), medical supplies (+15%), and surgical instruments (+8%) all increased in 2025.

The $6,200 Moment: What Jessica Actually Did

Let me show you how Jessica handled Max’s emergency—and why it worked:

Her situation:

- Dog needed $6,200 surgery immediately

- Had $800 in a checking account

- But she’d prepared three months earlier

Her preparation:

- Pet insurance (Healthy Paws): $42/month

- Policy: $250 deductible, 90% reimbursement, no annual cap

- Had already met the deductible from the previous visit

Her math:

- Total bill: $6,200

- Insurance covers: 90% = $5,580

- She pays: $620

What she did:

- Put the full $6,200 on CareCredit (0% for 18 months)

- Submitted claim Monday morning

- Got reimbursed $5,580 by Friday

- Paid off CareCredit immediately

Total out-of-pocket: $620 instead of $6,200.

That’s the difference between “we can save him” and “I don’t know if we can afford this.”

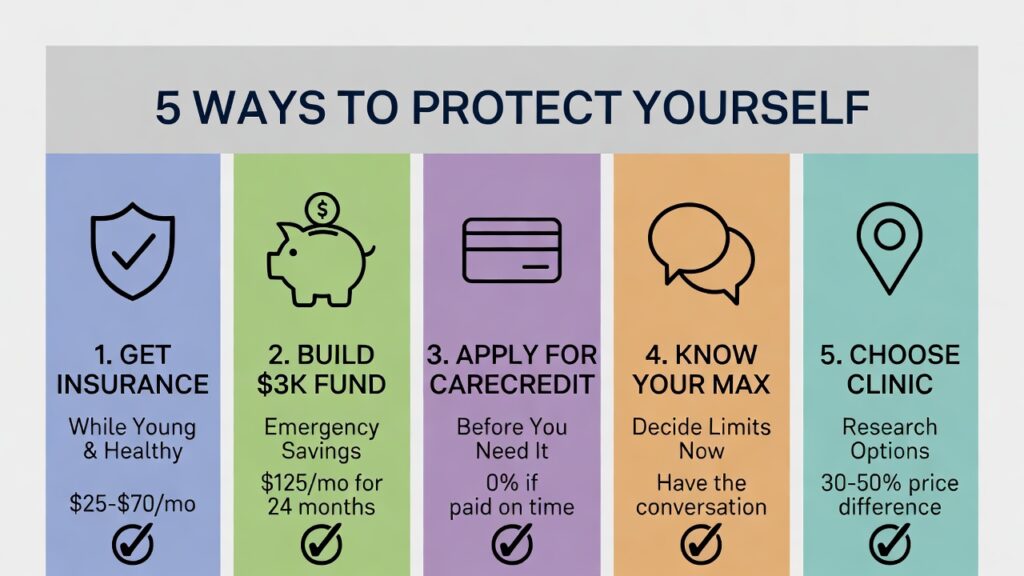

5 Strategies Smart Pet Owners Use

Strategy 1: Get Insurance While They’re Young and Healthy

The timing mistake: Waiting until pets are older or already sick.

The smart move: Enroll puppies/kittens under 6 months:

- Lowest premiums ($25-$40/month)

- No medical history to exclude

- Lock in rates before age increases

Best providers for emergencies:

| Provider | Best For | Monthly Cost | Claim Speed |

|---|---|---|---|

| Healthy Paws | No annual caps | $45 | 2-3 days |

| Trupanion | Direct-to-vet payment | $50+ | At checkout |

| Lemonade | Lowest cost | $31 | Instant (50%) |

| Pumpkin | Emergency urgent pay | $68 | 15 minutes |

Strategy 2: Build a $3,000 Emergency Fund

Why $3,000? Covers 80% of common emergencies, and your deductible if you have insurance.

How to save it painlessly:

- Automatic transfer: $125/month = $3,000 in 24 months

- Accelerated: $250/month = $3,000 in 12 months

- Bare minimum: $50/month = $600 in 12 months (better than nothing)

Pro tip: Put it in a high-yield savings account (4.5-5% APY) named “[Pet’s Name] Emergency Fund.” If it’s in your regular account, you’ll spend it.

Strategy 3: Apply for CareCredit NOW (Before You Need It)

What it is: Healthcare credit card offering 0% interest for 6-24 months. Accepted at 90% of U.S. vets.

Why apply before an emergency: They don’t approve people in crisis. The application takes 10 minutes, and approval is instant.

How to use correctly:

- Use for an emergency bill

- Submit the insurance claim immediately

- Get reimbursed

- Pay off CareCredit before promo ends

- Result: $0 interest

The horror story: Tom borrowed $4,800 (18-month promo), paid $250/month for 17 months, had an emergency in month 18, and missed the final payment. CareCredit charged 26.99% retroactive interest on the original $4,800. He owed $6,100 after already paying $4,250.

Don’t be Tom. Pay it off before the deadline.

Strategy 4: Know Your “Maximum” Number Ahead of Time

Have this uncomfortable conversation now, not at 2 AM in a vet lobby:

Questions to answer together:

- What’s the maximum we can spend to save our pet? ($2,000? $5,000? $10,000? No limit?)

- What do we do if costs exceed that?

- Does the answer change based on the pet’s age?

- What treatments are we comfortable declining?

Making these decisions calmly, in advance, gives you clear boundaries, faster treatment decisions, and less guilt.

No judgment here. Everyone’s financial situation is different. What matters is knowing your limits before you’re tested.

Strategy 5: Choose the Right Emergency Clinic

Not all emergency vets charge the same. Corporate-owned specialty centers charge 30-50% more than independent clinics.

Before the emergency:

- Google “[your city] emergency vet”

- Call 3-5 clinics and ask about emergency exam fees

- Ask: “Are you independently owned or corporate?”

- Save numbers of the 2 most affordable

Money-saving question: “If we can’t afford full treatment tonight, what’s the minimum to stabilize my pet until we can see our regular vet Monday?”

Sometimes they can stabilize for $800 vs. full surgery for $5,000.

You can also compare today’s top providers in our updated Best Pet Insurance Companies 2026 guide.

The “I’m Completely Broke” Emergency Plan

If you can’t afford insurance or savings, here’s your bare-minimum safety net:

Accident-Only Insurance ($10-20/month)

Covers: Hit by a car, broken bones, poisoning, foreign objects, snake bites

Doesn’t cover: Illnesses, cancer, infections, chronic conditions

Who should get this: Anyone who can’t afford more but wants protection against common disasters.

Apply for Assistance

Organizations that help with vet bills:

- RedRover Relief: (916) 429-2457 – Emergency grants

- The Pet Fund: (916) 443-6482 – Non-routine care

- Brown Dog Foundation: Cancer treatment help

- Waggle: Crowdfunding for vet bills

Warning: Limited funds, long wait lists. Apply immediately, don’t count on approval.

Vet School Clinics

Veterinary schools offer care at 30-50% less than private clinics. Students perform procedures supervised by licensed vets. Not available for true emergencies (not 24/7), but great for surgeries and chronic care.

What NOT to Do (These Mistakes Cost Thousands)

❌ Don’t Wait “To See If It Gets Better.”

By the time symptoms are obvious, the condition is advanced and more expensive.

Example: Cat stops eating on Monday (early kidney disease, $800 to treat). The owner waits until Friday (kidney failure, $3,500 to treat). Cost of waiting: $2,700.

❌ Don’t Get Insurance Right Before Surgery

Most policies have 14-day waiting periods for illnesses. Enrolling on Tuesday and trying to claim Friday? Denied. This is fraud.

❌ Don’t Cancel Insurance When Money Gets Tight

Cancel in year 3, dog gets diabetes in year 4, re-enroll in year 5? Diabetes is now pre-existing—never covered. Lifetime cost of a diabetic dog: $1,200-$2,400/year.

Better: Switch to accident-only ($15-20/month) rather than canceling completely.

Real Stories: The Difference Preparation Makes

Rachel’s $3,200 Chocolate Emergency

Her beagle ate dark chocolate chips. Emergency estimate: $3,200.

She had: Pet insurance (Pumpkin, $52/month) + $1,200 emergency fund

What she paid: $250 (deductible) + 10% ($295) = $545 total

Got urgent pay reimbursement in 20 minutes. Without insurance: $3,200 on a credit card.

James’s $14,800 Cancer Treatment

Golden retriever diagnosed with lymphoma at age 7. Full chemo: $14,800.

He had: Pet insurance (Healthy Paws) since puppy, $44/month, no annual cap

What happened:

- Insurance covered: 90% = $13,320

- He paid: $1,480 total

- Dog went into remission, lived another 3 years

Without insurance: $14,800 + emotional devastation of potentially declining treatment.

Marcus’s Nightmare (No Happy Ending)

Lab ate a sock. Surgery: $6,200.

He had: No insurance, $400 savings, maxed credit cards

What happened:

- Borrowed $3,000 from parents

- Put $2,500 on CareCredit

- Couldn’t pay off in time

- Got retroactive interest

- Total cost: $8,100 over 2 years

Damaged credit, strained family relationships, years of guilt. This is what we’re preventing.

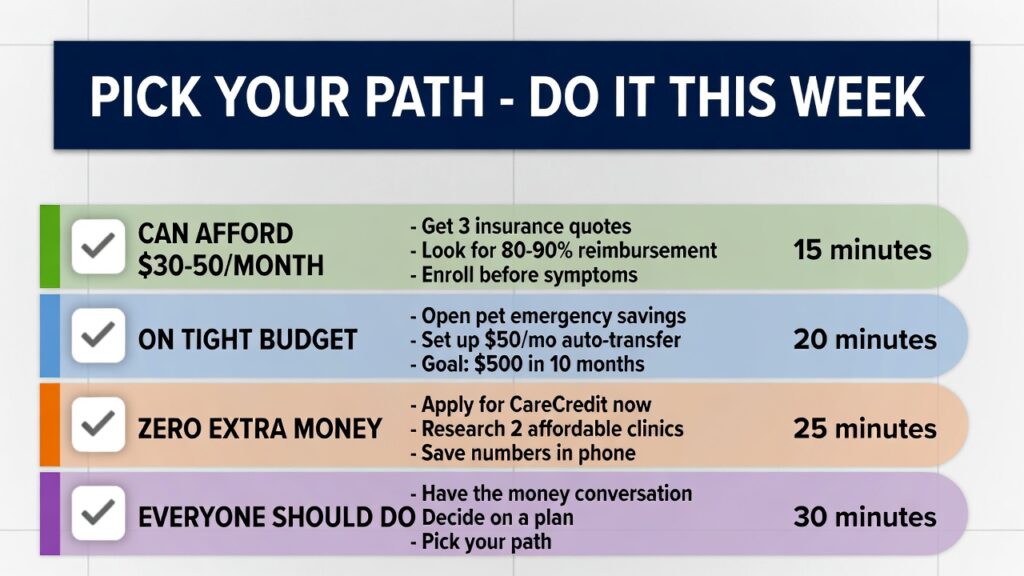

Your Action Plan: Do This Week

Pick ONE and do it in the next 7 days:

If You Can Afford $30-50/Month:

☐ Get 3 pet insurance quotes

☐ Look for 80-90% reimbursement, $250-500 deductible

☐ Enroll before symptoms appear

☐ Time: 15 minutes

If You’re on a Tight Budget:

☐ Open “Pet Emergency” savings account

☐ Set up automatic $50/month transfer

☐ Goal: $500 in 10 months

☐ Time: 20 minutes

If You Have Zero Extra Money:

☐ Apply for CareCredit (5 minutes)

☐ Research 2 affordable clinics near you

☐ Save their numbers in phone

☐ Time: 25 minutes

Everyone Should Do:

☐ Have “the money conversation.”

☐ Decide maximum emergency spend

☐ Write it down

☐ Time: 30 minutes

Frequently Asked Questions

Q: My pet is 9 years old with health issues. Can I still get insurance?

A: Yes, but current conditions are pre-existing (won’t be covered). NEW emergencies and conditions will be covered. Not ideal, but protects against future unknowns.

Q: Can I negotiate emergency vet bills?

A: Sometimes. What works: “Can we do a payment plan?” “What’s the minimum to stabilize tonight?” What doesn’t work: arguing about prices aggressively.

Q: Should I use GoFundMe for vet bills?

A: As a last resort. Try insurance, savings, CareCredit, and assistance organizations first. GoFundMe takes 3-7 days to get money—not good for “need surgery tonight.”

The Bottom Line

Emergency vet bills went up 18% this year. They’ll probably rise again next year.

You can’t control that.

But you can control whether you’re ready.

The people who don’t panic during emergencies aren’t richer. They just prepared: bought insurance when it was cheap, saved $100/month, applied for CareCredit they hoped never to use, and had awkward money conversations.

None of that is fun. None of it is Instagram-worthy.

But when their dog eats a sock at midnight, they make decisions based on what’s best for their pet—not what their credit card limit allows.

That’s the difference.

Questions? fursurely100@gmail.com |

Share this: Every pet owner should know this before an emergency.

📧 Email | 💬 Facebook | 🐦 Twitter

The cost of preparation: $30-50/month or 20 minutes.

The cost of being unprepared: $6,200 at 2 AM.

Choose wisely.

About FurSurely: We help U.S. pet owners understand real veterinary costs and find affordable protection. We work for you, not insurance companies.

Last Updated: February 16, 2026