The $5,000 Vet Visit: What Most Pet Owners Learn Too Late

Meta Description: One emergency vet visit can cost $5,000+. Learn what to expect, how to prepare, and the three strategies that protect your pet and your wallet (before it’s too late).

Reading time: 7 minutes

It’s 2 AM when your dog starts vomiting blood. You rush to the emergency vet, hands shaking. A technician hands you paperwork. Near the bottom, you see it:

“Estimated cost: $4,500 – $7,000”

You have $1,200 in checking. Your credit card has maybe $2,000 available. Nobody plans for this moment. But 84% of pet owners will face it.

I know because four years ago, I was sitting in that waiting room with my dog Riley, wondering if I could afford to save her life. That night cost me $4,200—and another $680 in credit card interest over 18 months.

Here’s what I wish someone had told me before that happened.

To understand which companies actually pay claims fast, see our guide to the best pet insurance providers in 2026.

What a $5,000 Emergency Actually Looks Like

Let me show you three real emergencies from the last 30 days:

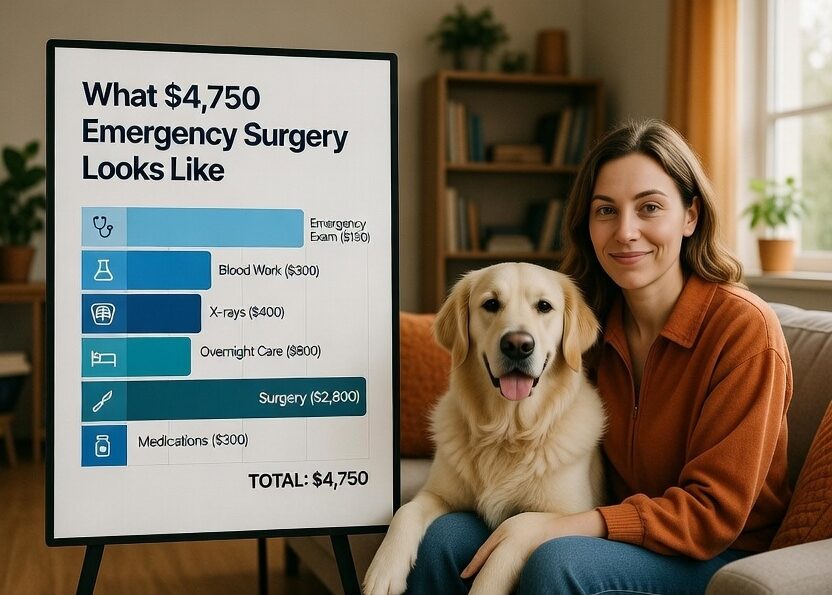

Charlie (3-year-old Lab): Ate a sock. Needed emergency surgery to remove it before his intestines ruptured.

- Total cost: $4,750

- Breakdown: Exam ($150) + X-rays ($400) + Overnight care ($800) + Surgery ($2,800) + Meds ($600)

Luna (9-year-old cat): Stopped eating, breathing fast. Diabetic crisis requiring 3 days in ICU.

- Total cost: $4,525

- What owners did: $2,000 on credit card, $1,500 on CareCredit, $1,000 borrowed from family

Max (7-year-old German Shepherd): Jumped off the deck, tore ACL. Needed orthopedic surgery.

- Total cost: $5,850

- What owners did: Had been saving $100/month for 2 years ($2,400 saved), paid the rest with a personal loan

These aren’t rare cases. These are the most common pet emergencies in America:

- Foreign body obstruction (dogs eating things): $3,000-7,000

- Hit by car/trauma: $3,500-15,000

- Cancer treatment: $10,000-20,000 over time

- ACL tears: $4,000-6,000 per leg

- Bloat emergency: $3,000-8,000

How Most People Handle It (And Why It Hurts)

When you need $5,000 and don’t have a plan, here’s what happens:

Credit cards (57% of people)

- Charge $5,000 at 21.5% interest

- Pay $200/month

- Total cost: $6,680 (you pay $1,680 in interest)

CareCredit (31% of people)

- Offers 0% interest for 6-18 months

- BUT: If you don’t pay it off in time, they charge 26.99% interest retroactively on the entire original balance

- Miss one payment? Same penalty

Borrow from family (23% of people)

- Strains relationships

- Creates guilt

- May take years to repay

Decline treatment (11% of people)

- Veterinarians call it “economic euthanasia.”

- Happens every day

- This is exactly why planning matters

The Three Strategies That Actually Work

After talking to hundreds of pet owners who’ve been through this, here are the approaches that consistently work:

Strategy 1: Pet Insurance (Best for Most People)

How it works:

- Pay $30-60/month

- When you have a vet bill, you pay upfront

- Submit receipts, get reimbursed 70-90%

Real math:

- Monthly premium: $45 (healthy 2-year-old Lab)

- Annual cost: $540

- Emergency surgery: $5,000

- You pay: $250 (deductible) + 10% ($475) = $725 total

- Insurance pays: $4,275

The catch: Enroll while your pet is healthy. Once they have a condition, it’s “pre-existing” and never covered.

Best for:

- Puppies/kittens (lock in low rates)

- Purebred dogs with genetic risks

- Anyone who can’t save $5,000 quickly

- People who want predictable costs

Top picks: Lemonade (instant claims, $31/month), Pumpkin (15-minute urgent pay), Trupanion (pays vet directly)

Strategy 2: Dedicated Emergency Fund (Best for Disciplined Savers)

How it works:

- Save $100-250/month in a separate account

- Target: $3,000 minimum, $5,000 comfortable

Timeline:

- $100/month = $3,000 in 2.5 years

- $250/month = $3,000 in 12 months

Best for:

- Stable income

- Naturally disciplined savers

- Senior pets (hard to insure)

The catch: Takes 1-3 years to build. You’re vulnerable during that time.

Strategy 3: Insurance + Savings Combo (Smartest Option)

How it works:

- Get insurance for major coverage

- Save $1,000-2,000 for deductibles

- Apply for CareCredit (but don’t use it yet)

Why it’s powerful: Your dog needs $6,000 ACL surgery on Saturday night.

- Pay vet $500 cash + $5,500 CareCredit

- Submit the claim on Monday

- Insurance pays you $5,100 within 48 hours

- Pay off CareCredit immediately

- Out of pocket: Just $900 total, zero interest

What I Wish I’d Known Before Riley Got Sick

I thought pet insurance was a scam. “I’ll just save the money myself,” I said.

Then Riley got pancreatitis. Three days hospitalized. $4,200.

I had $1,800 saved. Put $2,000 on a credit card. Borrowed $400 from my sister. Paid $680 in interest over 18 months.

Total cost: $4,880

Three months later? Riley tore her ACL. Another $5,200.

I finally got insurance. But you know what? Pancreatitis and ACL injuries are now pre-existing conditions.

Here’s what I wish someone had told me:

1. “Young and healthy” doesn’t mean “safe.” Most emergencies happen to young pets. That’s when they eat socks, get hit by cars, and tear ligaments.

2. The $30/month you “can’t afford” is nothing compared to the $5,000 you definitely can’t afford. I was “saving” $30/month by not having insurance. One emergency cost me 162 months of premiums. Over 13 years.

3. “I’ll save the money instead” only works if you actually do it. I said I’d save $50/month. After two years? I had $400. Life always got in the way.

4. The guilt is worse than the money. The worst part wasn’t the debt. It was sitting in that vet office, wondering, “What if this was $10,000? What would I do?”

Your Action Plan: What to Do This Week

Don’t bookmark this and forget about it. Take 30 minutes right now:

Option A: Get Insurance (If Your Pet Is Healthy)

☐ Get quotes from 3 providers

☐ Look for: 80-90% reimbursement, $250-500 deductible, accident + illness

☐ Enroll before any symptoms appear

☐ Cost: $30-60/month

Option B: Start Emergency Fund

☐ Open high-yield savings account (currently 4-5% interest)

☐ Name it “[Pet’s Name] Emergency Fund”

☐ Set up automatic $100/month transfer

☐ Add any windfalls (tax refund, bonus)

☐ Goal: $3,000 minimum

Option C: Hybrid Approach (Best)

☐ Get basic insurance ($30-40/month)

☐ Save $1,000 for deductibles

☐ Apply for CareCredit now (before you need it)

☐ Total monthly cost: $30-40 + whatever you can save

Real Costs: What to Expect in 2026

Diagnostics alone (before treatment):

- Emergency exam: $150-250

- Blood work: $250-450

- X-rays: $300-500

- Total just to find out what’s wrong: $500-1,000

Common emergencies:

- Foreign body surgery: $3,000-7,000

- Broken leg: $2,500-4,000

- Hit by car (moderate): $3,500-10,000

- Poisoning: $500-5,000

- Pancreatitis ICU: $2,000-5,000

Geographic variation:

- Rural areas: $2,800-4,000 (same surgery)

- Urban areas (NYC, SF, LA): $6,500-7,200

Questions You’re Asking Right Now

Q: My dog needs emergency surgery NOW, and I don’t have money. What do I do?

Immediate options:

- Apply for CareCredit (carecredit.com) – 10-minute approval

- Ask the vet about payment plans

- Call RedRover Relief: (916) 429-2457

- Create a GoFundMe immediately

- Ask vet: “What’s the minimum to stabilize my pet?”

Q: Is insurance worth it, or should I just save?

The math:

- Save $75/month for 5 years = $4,500 saved, one emergency wipes it out

- Pay $45/month insurance for 5 years = $2,700 spent, but $5,000 emergency costs you just $750

Real question: Can you save $75/month and NOT touch it?

- If yes → Self-insure

- If no → Get insurance (forces you to save)

Q: My pet is 8 years old. Too late for insurance?

Not too late, but:

- Premiums will be higher

- Current conditions are pre-existing

- But you CAN still cover future injuries and new illnesses

Q: What if I can’t afford treatment?

I’m so sorry. Before deciding:

- Ask for the vet’s social worker

- Ask about surrender programs (some vets will take ownership and treat)

- Call breed-specific rescues

- Be honest with your vet about financial limits

This is not your fault. Economic euthanasia is real.

The Bottom Line

You have something most pet owners don’t have when they’re in that emergency room at 2 AM: time to prepare.

You don’t have to choose between your savings and your dog’s life. You don’t have to call your parents crying, asking for money.

You can plan for this.

Not because you’re paranoid—because you love your pet enough to think ahead.

Do One Thing Today

Get insurance quotes OR open an emergency savings account with $100

Pick one. Do it now.

Because the day you need it, you’ll be so grateful you did.

Questions? fursurely100@gmail.com

Share this: Every pet owner should read this before an emergency happens.

📧 Email | 💬 Facebook | 🐦 Twitter

About author: I’m not a financial advisor—just a pet owner who learned this the expensive way. This reflects my experience and research. Consult professionals for your situation.

About FurSurely: We help pet owners find affordable insurance and plan for real costs. We work for you, not insurance companies.

Last Updated: February 15, 2026