US Pet Insurance Industry Surpasses $4.7 Billion — What It Means for Pet Owners in 2026

Imagine Sarah, a Golden Retriever owner in New York. When her dog, Cooper, swallowed a stray tennis ball, the emergency surgery bill hit $5,000. Sarah didn’t have to choose between her savings and Cooper’s life because she was part of a record-breaking trend.

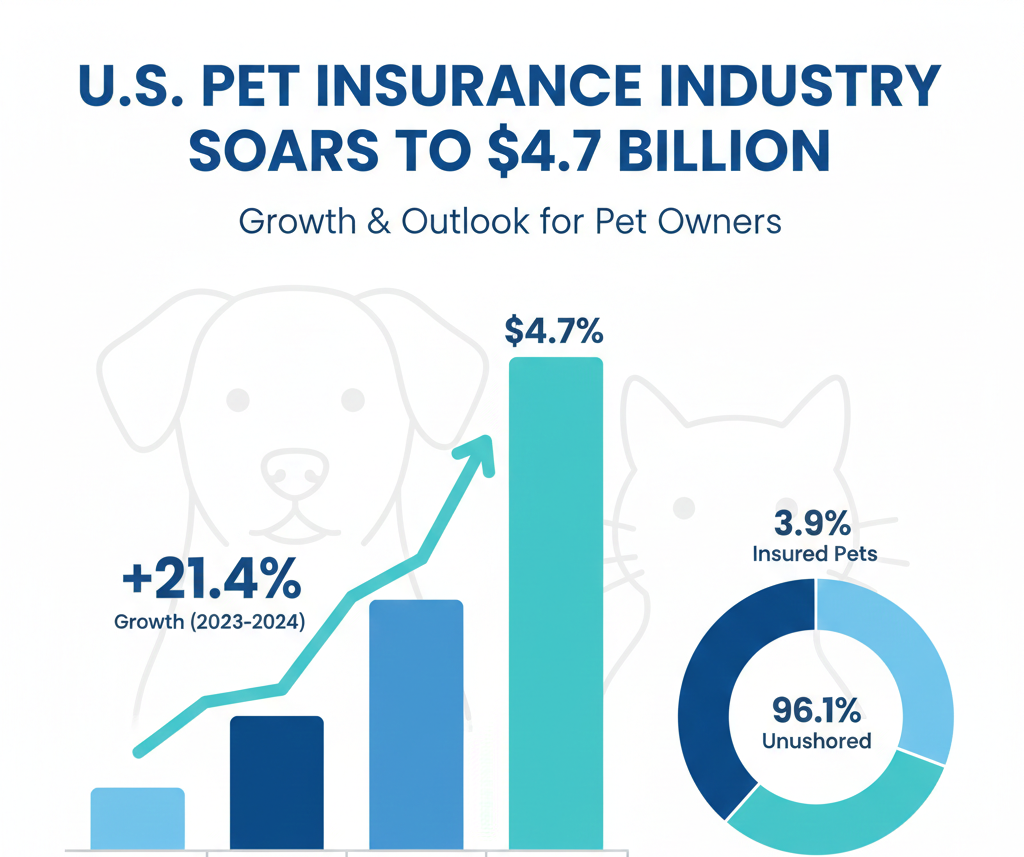

In 2024, the U.S. pet insurance industry officially surpassed $4.74 billion in total premiums (the money pet owners pay for coverage). This isn’t just a corporate milestone; it represents a massive shift in how we care for our “fur babies.” As we move through 2026, pet insurance has moved from a “nice-to-have” luxury to an essential tool for household financial survival.

Quick Takeaways for 2026

The Market is Doubling: The industry has more than doubled since 2020 as more owners realize that “economic euthanasia” (having to put a pet down because of cost) is a risk they aren’t willing to take.

Costs are Rising: Veterinary prices rose over 8% recently, making insurance even more critical for predictable budgeting.

Better Tech: Most providers now offer mobile apps for 2-day claim processing or even “Direct Pay” where the insurer pays the vet at checkout.

The Growing Boom: Why Now?

The U.S. pet insurance market has exploded, growing by over 20% every single year for the past five years. Today, over 6.4 million pets in the U.S. are insured.

| Year | Total Money Paid (GWP) | Growth Rate | Total Insured Pets |

| 2024 | $4.74 Billion | 21.4% | 6.4 Million |

| 2023 | $3.91 Billion | 21.4% | 5.7 Million |

| 2022 | $3.22 Billion | 24.2% | 4.8 Million |

| 2020 | $1.99 Billion | 27.5% | 3.1 Million |

While the market is massive, only about 3.9% of pets in the U.S. have coverage. In countries like Sweden, nearly 90% of dogs are insured. This means the U.S. market is still in its early stages, and competition between companies is heating up, which is great news for your wallet.

If you’re new to how policies work, read our guide on how pet insurance works for beginners in the USA.

The “Veterinary Buffer”: Saving More Than Just Money

For many, the most stressful part of pet ownership is the “money talk” at the vet. A 2025 study found that vets have these difficult conversations at least four times every week.

When a pet is insured, the emotional weight of the clinic visit changes. Instead of asking “How much will this cost?”, owners can ask “What is the best way to help my pet?”

Compliance: Insured owners are 68% more likely to follow through with expensive treatments.

Better Outcomes: Nearly half of all vets report that insurance leads to better health results for the pets they treat.

Stopping Economic Euthanasia: 1 in 3 vets have seen a reduction in price-driven euthanasia because of insurance.

Real-World Scenarios: What High-End Care Actually Costs

Modern medicine for pets now mirrors human healthcare. Without insurance, these “catastrophic” bills often end up on high-interest credit cards.

The $10,000 Back Surgery (Dachshunds & IVDD)

Dachshunds are prone to Intervertebral Disc Disease (IVDD), a back issue that can cause paralysis.

The Story: A Dachshund named “Dash” suddenly loses the use of his back legs.

The Bill: MRI ($2,500) + Emergency Surgery ($4,000) + 4 days of hospital care ($2,500) + Rehab ($1,000) = Total $10,000.

With Insurance (90% Reimbursement): After a $250 deductible, the owner pays roughly $1,225 instead of $10,000.

The $7,000 Heart Crisis (Maine Coons & HCM)

Maine Coons are famous for their size, but they often struggle with Hypertrophic Cardiomyopathy (HCM), a thickening of the heart muscle.

The Bill: Stabilization of heart failure can cost $7,000 in emergency visits.

Chronic Care: Ongoing medications and ultrasounds can cost $100 to $250 per month.

Top Provider Comparison (2026 Rankings)

With over 30 companies competing, choosing a plan can be overwhelming. Here are the top performers based on recent consumer sentiment and coverage features.

| Provider | Best For… | Key Perk | Typical Waiting Period |

| Pets Best | Overall Value | Direct pay to vet available. | 3 days (Accident) / 14 days (Illness) |

| Spot | All-Around Coverage | Covers exam fees & behavioral issues. | 14 days for all |

| Figo | Tech & Upgrades | 100% reimbursement option. | 1 day (Accident) / 14 days (Illness) |

| Chewy (w/ Trupanion) | Ease of Use | Pays vet directly at checkout. | 0 days (Accident) / 30 days (Illness) |

| Lemonade | Budget/Discounts | Fast AI-driven claims. | 2 days (Accident) / 14 days (Illness) |

| Embrace | Healthy Pets | Deductible drops if you don’t claim. | 2 days (Accident) / 14 days (Illness) |

Strategic Implications: What to do TODAY

The $4.7 billion milestone proves that insurance is maturing, but you need to be strategic to avoid “gotchas.”

1. The “Age” Rule

Enroll your pet before their first birthday. Because insurance rarely covers “pre-existing conditions,” waiting until your dog is limping means that injury—and anything related to it—will be excluded forever.

2. Watch for the “Bilateral” Red Flag

Many policies have a hidden rule: if your pet has a hip or knee issue on the left side before you sign up, they will never cover a similar issue on the right side. Check your policy for “Bilateral Exclusions” before signing.

3. Use the “DTC” Advantage

Direct-to-consumer (DTC) digital platforms are now the largest sales channel. Use marketplaces like Policy Advisor to compare multiple quotes side-by-side. This ensures you aren’t overpaying for the brand name.

Pet Owner’s Action Checklist:

[ ] Audit Your Breed: Does your pet have a genetic risk (e.g., Bulldogs and breathing, Labs and hips)? Ensure your plan covers “Hereditary Conditions.”

[ ] Check the Waiting Period: Most plans have a 6-month wait for orthopedic issues. Can you waive this with a vet exam?

[ ] Evaluate “Direct Pay”: Can you afford to front a $5,000 bill and wait weeks for a check? If not, prioritize providers like Trupanion or Chewy.

[ ] Review Multi-Pet Discounts: If you have more than one pet, look for a “Family Plan” with a shared deductible.

Frequently Asked Questions (FAQ)

Q: Is pet insurance worth it if I have savings?

A: It depends on your risk tolerance. Insurance turns an unpredictable $10,000 shock into a predictable $50 monthly bill. Even with savings, insurance ensures those funds stay in your retirement or emergency fund.

Q: Does pet insurance cover routine shots? A: Standard plans usually don’t, but most companies offer a Wellness Add-on for about $15–$25 per month that covers vaccines, flea prevention, and dental cleanings.

Q: Can I change companies later?

A: You can, but it’s risky. Any health issue your pet had while with Company A will be considered a “pre-existing condition” by Company B and won’t be covered.

Q: What is a “Waiting Period”? A: It’s the time between when you buy the policy and when you can actually file a claim. Typically, it’s 3 days for accidents and 14 days for illnesses.

Q: Do premiums go up every year? A: Yes. As your pet ages, the risk of illness increases. Expect your monthly payment to rise slightly each year—this is the “birthday pricing” trend.

Conclusion

The U.S. pet insurance industry’s leap to $4.7 billion isn’t just a number on a corporate earnings report—it’s a reflection of a hard truth that millions of pet owners have already learned: modern veterinary care can save your pet’s life, but it can also devastate your finances without warning.

Sarah’s story with Cooper isn’t unique. Every day, thousands of pet owners face the same choice: drain their emergency fund, max out credit cards, or make an impossible decision at the vet’s office. The difference in 2026 is that you don’t have to face that choice alone.

With veterinary costs rising over 8% annually and emergency surgeries routinely hitting $5,000 to $15,000, the question isn’t whether you can afford pet insurance—it’s whether you can afford to go without it. The 6.4 million pet owners who enrolled last year understood something critical: a $50 monthly premium is infinitely easier to budget than a $10,000 surprise bill.

Your Next Steps:

The data is clear, the options are better than ever, and the stakes are your pet’s life. Here’s what to do right now:

- Don’t wait for a diagnosis. Pre-existing conditions are never covered. If your pet is healthy today, that’s your window.

- Get three quotes. Use comparison tools like Policy Advisor to see side-by-side pricing. Don’t assume the biggest brand is the best deal.

- Read the fine print on waiting periods. If your breed is prone to hip or knee issues (Labs, Golden Retrievers, German Shepherds), ask if you can waive the 6-month orthopedic waiting period with a vet exam.

- Prioritize “Direct Pay” if cash flow is tight. Companies like Trupanion and Chewy pay the vet at checkout, so you’re not fronting thousands of dollars while waiting for reimbursement.

The $4.7 billion milestone proves that pet insurance has moved from the fringes to the financial mainstream. The only question left is: will you be part of the next wave of smart pet owners who protect both their pets and their wallets—or will you be the one scrambling for options when the emergency hits?

Cooper got his surgery. Dash can walk again. Your pet deserves the same chance.

Start comparing quotes today, because the best time to get insurance was yesterday. The second-best time is right now.

Compare top providers in our full Top Pet Insurance Providers for 2026 comparison guide.